How AI and Automation Are Changing Loan Management Systems in 2026

- Arpan Desai

- Dec 15, 2025

- 3 min read

Updated: Jul 2

AI and automation in loan management systems are transforming lending by streamlining loan origination, underwriting, approval, and repayment processes. These technologies reduce manual work, improve credit decision accuracy, detect fraud in real time, and enhance customer experience. By integrating AI-driven analytics and automation workflows, financial institutions can process loans faster, reduce operational costs, and ensure more compliant and data-driven lending decisions. |

1. Introduction: The AI-Driven Evolution of Loan Management

In the United States, financial institutions are facing unprecedented demand for speed, compliance, and scalability. Traditional loan management systems, often reliant on spreadsheets and manual workflows, can no longer keep up. Enter AI and automation in loan management systems—a revolution that promises faster processing, reduced errors, and smarter lending decisions.

Banks using AI-driven loan management see 50–70% faster processing times, improved risk monitoring, and more satisfied borrowers.

FintegrationFS is helping fintech startups, banks, and lenders leverage advanced loan servicing software, loan origination systems, and automated loan processing software to build scalable, secure, and compliant lending platforms. Explore our loan management solutions.

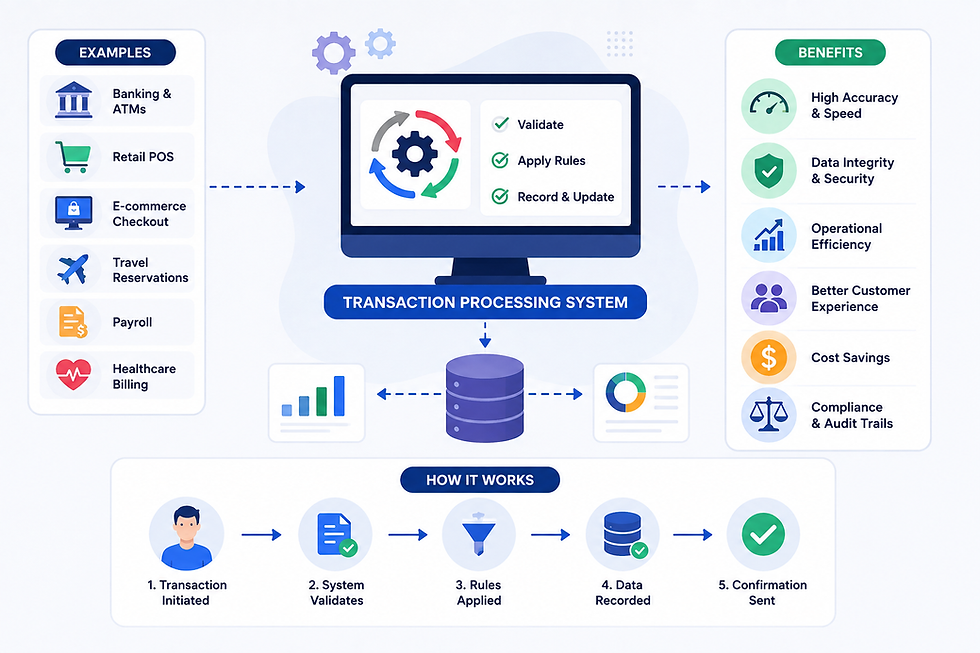

2. What Are Loan Management Systems (LMS)?

A loan management system (LMS) is software designed to manage the full lifecycle of a loan, from origination to servicing and collection. Modern systems are evolving to integrate AI and automation, giving institutions a competitive edge.

Core LMS functions:

Loan application management

Borrower onboarding and verification

Payment tracking and amortization

Compliance reporting and risk assessment

Traditional LMS vs Modern AI-Powered LMS:Traditional LMS often requires manual approvals and data entry. AI-powered systems integrate predictive analytics, workflow automation, and real-time monitoring to reduce errors and speed up approvals.

3. Role of AI in Loan Management Systems

AI is transforming loan management systems by:

Improving borrower assessment accuracy with predictive credit scoring

Detecting fraud and anomalies using machine learning

Automating underwriting and loan decision-making

Offering personalized lending recommendations and predictive repayment analysis

Imagine having an assistant who can analyze thousands of loan files in minutes, detect risk patterns, and make data-driven decisions—without coffee breaks.

4. Role of Automation in Loan Lifecycle

Automation reduces repetitive manual tasks:

Document verification using AI and OCR

Workflow automation for approvals, notifications, and reminders

Integration with banking APIs for real-time payment updates

Benefits:

Faster loan disbursement

Reduced errors

Improved borrower experience

This combination of AI and automation turns traditional mortgage management software and personal loan management platforms into smart, scalable, and efficient solutions.

5. Key Features of AI & Automation-Driven Loan Management Systems

Intelligent borrower scoring and eligibility analysis

Real-time risk assessment

Automated loan origination and documentation

Payment scheduling and auto-collection

Compliance and regulatory monitoring

Analytics dashboards for lenders

Chatbots and AI customer support

6. Benefits for Lenders and Borrowers

Lenders

Reduced processing costs

Faster decision-making

Improved risk management

Better compliance adherence

Borrowers

Faster approvals

Transparent loan tracking

Personalized offers

Reduced paperwork

7. Trends in AI & Automation for Loan Management (2026)

Predictive analytics for credit risk

Hyper-personalized lending offers

Integration with fintech APIs (Plaid, Codat, etc.)

Cloud-native LMS for scalability

Mobile-first borrower experiences

8. Challenges and Considerations

Compliance with US laws (FCRA, ECOA)

Data privacy and cybersecurity

Maintaining transparency in automated decisions

Integrating AI/automation with legacy systems

9. Future Outlook

Fully automated loan lifecycle in 2026–2030

AI-driven portfolio optimization

Embedded finance: loans in apps using APIs

Continuous learning AI improving credit decisions

Conclusion

AI and automation in loan management systems are essential for US fintech startups, banks, and wealthtech companies looking to scale and reduce operational inefficiencies.

Explore FintegrationFS Loan Management System solutions to see how your institution can leverage AI-powered LMS for faster, smarter, and compliant lending.

FAQs

What is AI and automation in loan management systems?

Software that uses AI and workflow automation to manage loans efficiently, from origination to servicing.

How does AI improve loan processing?

AI predicts credit risk, detects fraud, and automates underwriting for faster, more accurate decisions.

What tasks can automation handle in LMS?

Document verification, payment scheduling, compliance checks, and borrower notifications.

Who benefits from AI-powered loan management?

Banks, fintech startups, lenders, wealthtech companies, and borrowers looking for faster approvals.

How does AI reduce risk in loan portfolios?

It monitors patterns, predicts defaults, and flags high-risk borrowers proactively.

Can AI LMS integrate with banking APIs?

Yes, it can connect to Plaid, Codat, ACH, and other financial data providers.

What are key features of modern LMS?

Automated origination, borrower scoring, risk monitoring, analytics, compliance tracking.

Is AI in LMS compliant with US regulations?

Yes, systems are built to comply with FCRA, ECOA, and other federal/state laws.

How does AI improve borrower experience?

Faster approvals, personalized offers, real-time tracking, and reduced paperwork.

Why choose FintegrationFS for LMS?

Because we build secure, compliant, scalable AI-powered loan management systems for fintech and banking clients in the USA.