What Is an Investment Platform? Complete Guide for Fintech Founders

- Arpan Desai

- Mar 5

- 5 min read

Updated: Mar 5

An investment platform is a digital product that lets users invest in financial assets-like stocks, ETFs, mutual funds, bonds, crypto (where permitted), or alternative assets—through a web or mobile experience. For fintech founders, building an investment product is not just about UI and trading buttons. It’s about trust, compliance, performance, data accuracy, and a rock-solid backend that can handle money movement, order flows, and reporting.

This guide is written for builders who want practical clarity: what modules you need, how the end-to-end workflow works, and which architecture, security, logging/audit, and deployment practices matter most—especially if your target industry is custom investment software development.

You’ll also see where partners like a fintech software development company, finTech developers, or a plaid developer typically fit into the build.

Why founders build an investment platform

Founders typically build an investment platform to:

Offer investing inside an existing product (embedded investing)

Launch a brokerage-like experience (stocks/ETFs/options depending on region)

Build goal-based investing (wealth, retirement, education)

Provide managed portfolios (robo-advisory)

Create a curated marketplace (private deals, fractional investing where allowed)

Deliver an “investment solution” for a niche audience (athletes, creators, expats, SMEs)

The upside is huge—but so are the stakes: a single calculation bug, missing audit trail, or weak security control can break user trust and create regulatory headaches.

Core Modules of an Investment Platform (What You Must Build)

A modern investment platform usually includes these modules. The exact set depends on your product model (brokerage, advisor, marketplace, robo, etc.).

1) Onboarding + Identity (KYC/KYB)

User registration + profile

KYC or KYB verification (region-specific)

Risk profiling/suitability questionnaire (often required)

Consent + disclosures storage

2) Account & Portfolio Management

Investment account creation

Holdings view (positions, cost basis, P&L)

Portfolio performance charts and breakdowns

Tax lots (where applicable)

3) Market Data + Asset Discovery

Instruments master (symbols, ISINs, fund identifiers)

Search, watchlist, filters

Price feeds + corporate actions (splits, dividends)

4) Order & Trade Lifecycle (if you support trading)

Quote retrieval

Place order (market/limit; others as allowed)

Order status tracking (pending, filled, partial, cancelled)

Trade confirmations

5) Funding, Withdrawals & Money Movement

Bank linking (often via a plaid developer in supported regions)

Deposits and withdrawals

Ledger and reconciliations

Payment rails integration (region-specific)

6) Compliance + Disclosures + Reporting

Activity statements

Confirmations

Regulatory reporting (depends on license + jurisdiction)

Policy enforcement: trading windows, suitability rules, restricted lists

7) Support + Ops Console

Admin dashboard

Customer support tools

Manual review queues (KYC exceptions, disputes)

Audit viewer (who changed what and when)

8) Notifications

Order status notifications

Price alerts, dividend alerts

Risk alerts/compliance notices

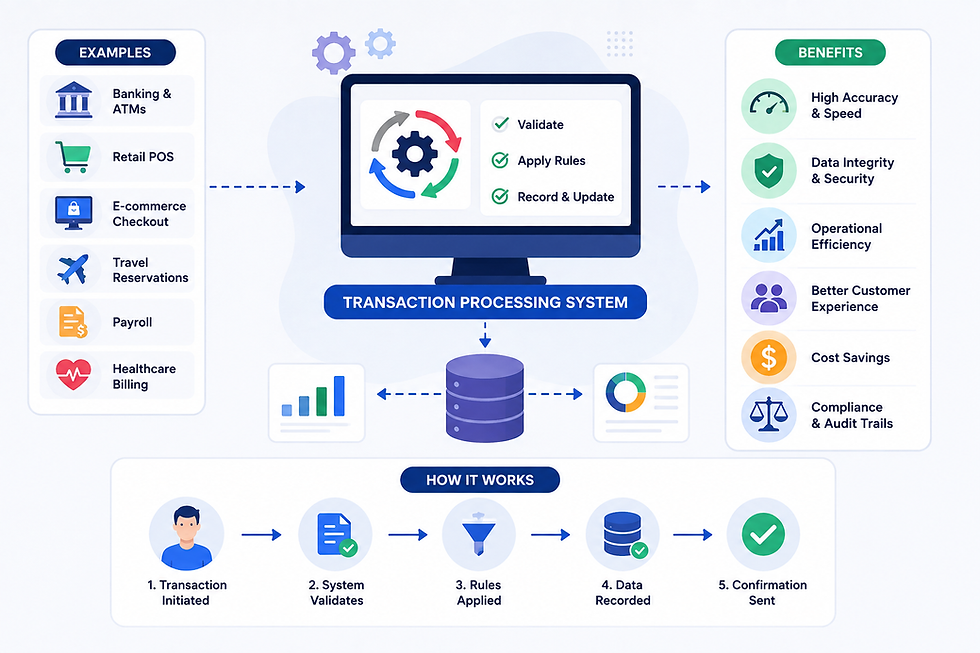

Step-by-Step Workflow: How an Investment Platform Works

Step 1: User signs up + completes KYC

The platform verifies identity, stores disclosures, and sets account eligibility.

Step 2: User links a bank account + funds account

Users deposit money. Integrations can power bank connectivity—this is where a plaid developer is commonly used for bank linking and verification.

Step 3: User discovers an asset and places an order

The platform:

Retrieves price/quote

Validates trading rules (suitability, restricted assets, limits)

Creates an order request

Step 4: Order is routed and executed

Depending on your model, the order may go to:

A broker/dealer or exchange partner

An internal execution engine (rare, regulated)

A third-party investment provider

Step 5: Portfolio updates + confirmations generated

Once executed:

Holdings update

Transaction history records the trade

Confirmation documents are generated

Notifications are sent

Step 6: Ongoing portfolio servicing

The platform handles:

Corporate actions (dividends, splits)

Performance calculations

Statements and reports

Withdrawals and transfers

Architecture Patterns for Building an Investment Platform

Because you’re dealing with money and high trust, architecture matters.

Pattern 1: Modular Monolith (Best for MVP → scale)

A clean modular monolith is often best early:

Faster development

Fewer operational headaches

Easier debugging

You still separate code by domains:

Onboarding

Accounts/Portfolio

Orders/Trades

Market Data

Funding/Ledger

Reporting/Compliance

This is a common approach used by a fintech software development company to deliver MVPs quickly without sacrificing long-term scalability.

Pattern 2: Service-Oriented + Event-Driven (Best for growth)

When volume grows, split into services:

Orders Service

Portfolio Service

Ledger Service

Market Data Service

Reporting Service

Use events like:

DepositPosted

OrderPlaced

OrderFilled

DividendReceived

Event-driven systems improve traceability and keep reporting accurate.

Pattern 3: Ledger-First Architecture (Strongest for auditability)

A ledger-first model means:

Every money movement is an immutable event

Balances are derived from the ledger

You can reproduce account state for disputes and audits

This is a best practice borrowed from Digital Banking Software Development where traceability is non-negotiable.

Security Controls

A secure investment platform protects both user funds and system integrity.

Identity & Access

MFA for admin and support teams

RBAC (Role-based access control)

Maker-checker approvals for high-risk ops actions (withdrawals, account edits)

Session management + device controls

Data Protection

TLS in transit

Encryption at rest (DB + file storage)

Field-level encryption for sensitive data (IDs, bank tokens)

Secrets manager for API keys

Transaction Safety

Idempotency keys for deposits/withdrawals/orders

Rate limits and bot protection

Fraud signals (velocity checks, unusual login patterns)

Webhooks verification (signature validation)

Platform Hardening

WAF + DDoS protection

Dependency scanning (SCA)

Container scanning if using Docker/Kubernetes

Security testing in CI/CD

Your finTech developers should treat security as part of the product—not a checklist at the end.

Logging, Audit Trails, and Monitoring

If there’s a dispute (“I didn’t place that order” / “my withdrawal failed”), logs and audit trails are how you resolve it.

What to log

Authentication events (login, failed login, MFA)

Order lifecycle (created, updated, cancelled, filled)

Money movement events (deposit, withdrawal, reversal)

Admin actions (any manual change)

Provider interactions (API requests/responses with correlation IDs)

Audit trail rules

Append-only audit logs (tamper-resistant)

Capture: actor, timestamp, IP/device, before/after

Store correlation IDs across services

Keep retention policies aligned with regulations

Monitoring that actually helps

Order failure rate spikes

Withdrawal failure rate

Provider API downtime

Ledger mismatch alerts (reconciliation failures)

Latency and error dashboards

Deployment Best Practices (So You Don’t Break Trust)

A slow platform is bad. A wrong balance is worse.

Environment setup

Separate dev/staging/prod

No production secrets in staging

Masked data for testing

Release strategy

Blue-green or canary deployments

Feature flags for risky releases

Automated rollback on high error rates

Reliability essentials

Database backups + restore testing

Incident runbooks

Disaster recovery plan (even a lightweight one)

Load testing around peak events (market open, major news)

Many teams building Fintech app Development products pair backend reliability with polished frontends from a mobile app development company.

Build vs Buy: A Founder’s Quick Decision Guide

You can either:

Build the full stack (more control, more time)

Use regulated partners for execution/custody and build the UX + orchestration

Most founders start by integrating partners and building the core experience + ledger + reporting layer as their defensible product, especially for a specialized investment solution.

FAQs

1) What is an investment platform in fintech?

An investment platform is a digital system that allows users to invest in financial products (like stocks, ETFs, funds, bonds, or alternatives), track portfolios, fund accounts, and access reporting in one place.

2) What’s the difference between an investment platform and a trading app?

A trading app is usually focused on placing trades. An investment platform is broader: onboarding, funding, portfolio management, reporting, compliance, and often advisory or goal-based investing.

3) What are the must-have components for custom investment software development?

Core components include KYC onboarding, funding and withdrawals, portfolio accounting, order lifecycle (if trading), market data, ledger and reconciliation, reporting, admin tools, and audit logs.

4) Why is a ledger important in investment products?

A ledger creates a traceable history of every balance-affecting event. It helps prevent disputes, supports reconciliation, and strengthens compliance.

5) How do you keep an investment platform secure?

Use MFA, RBAC, encryption, idempotent APIs for transactions, webhook verification, strong monitoring, and immutable audit logs. Regular security scans and staged deployments reduce risk.