How a Modern Loan Management System Transforms Digital Lending in India & the US

- Arpan Desai

- Dec 4, 2025

- 4 min read

Updated: Feb 2

Digital lending has changed more in the last five years than it did in the previous two decades. Customer expectations are higher, competition is intense, and compliance requirements are constantly evolving. Whether you’re a fintech startup in Bengaluru or a lending institution in New York, you now need more than just a loan dashboard—you need a modern, intelligent, and scalable way to run your lending operations.

This is where a loan management system becomes the backbone of your entire lending workflow. A modern LMS doesn’t just track EMIs or store customer profiles; it transforms the entire lending lifecycle—origination, underwriting, KYC, disbursement, compliance, collections, reporting, and customer experience.

In this article, we explore how next-generation LMS platforms are driving transformation across India and the US, and why modern lenders are rapidly adopting tools such as digital lending system, loan automation system, AI-powered loan management system, and cloud-based loan management system.

Why Traditional Lending Systems No Longer Work

Legacy systems were built for branch-based operations, predictable customer

behavior, and manual workflows. But today:

Customers expect decisions in minutes, not days.

Regulators expect real-time compliance.

Fraud patterns evolve weekly.

Lending is shifting from offline to embedded experiences.

A traditional LMS cannot match this pace. Most lenders face challenges like:

Manual onboarding and document checks

Delayed underwriting decisions

No centralized risk visibility

High operational cost

Poor scalability

Compliance gaps (RBI in India; FDIC/CFPB in the US)

Modern lending demands speed, automation, accuracy, and compliance—without increasing risk. That’s where a new-age loan management system becomes mission-critical.

How a Modern LMS Is Transforming Digital Lending

1. End-to-End Automation Across Borrower Lifecycle

A modern loan management software automates every stage—from onboarding to final closure. With integrations like Aadhaar, PAN, DigiLocker (India) and KYC/AML, OFAC, SSN verification (US), lenders reduce approval times drastically.

Automation also includes:

Document collection

Credit bureau pulls

Underwriting rules

Repayment reminders

NPA alerts

Collection workflows

This eliminates manual errors and reduces operational load by up to 70%.

2. Instant, Smarter Decisioning with AI & Rule Engines

Fintech leaders are moving towards AI-powered loan management system models that combine rule-based engines with machine learning. AI models evaluate:

Income stability

Behavioural signals

Fraud indicators

Creditworthiness

Repayment probability

As a result:

Underwriting becomes faster

Approval accuracy improves

Bad debts decrease

Operational overhead reduces

AI is no longer optional—it’s the competitive moat for lenders in both India and the US.

3. Faster and Compliant Customer Onboarding

India and the US operate in heavily regulated environments. A fully compliant digital lending system integrates:

India:

Aadhaar eKYC

PAN verification

Account Aggregator

GST & DigiLocker

CKYC

Bureau APIs: CIBIL, CRIF, Experian

US:

SSN verification

OFAC checks

KYC/AML services

Bank verification (Plaid, MX)

E-signature and ID verification

Fraud prevention APIs

A modern LMS ensures that lenders stay aligned with regulations such as:

RBI Digital Lending Guidelines (India)

FDIC, CFPB, GLBA, AML rules (US)

4. Cloud Scalability for Growing Fintechs

A cloud-based loan management system allows lenders to scale effortlessly. Instead of worrying about servers, downtime, or data limits, lenders get:

99.9% uptime

Auto-scaling infrastructure

Secure multi-region backups

High availability

Faster deployments

This is especially important for fintechs building cross-border lending models.

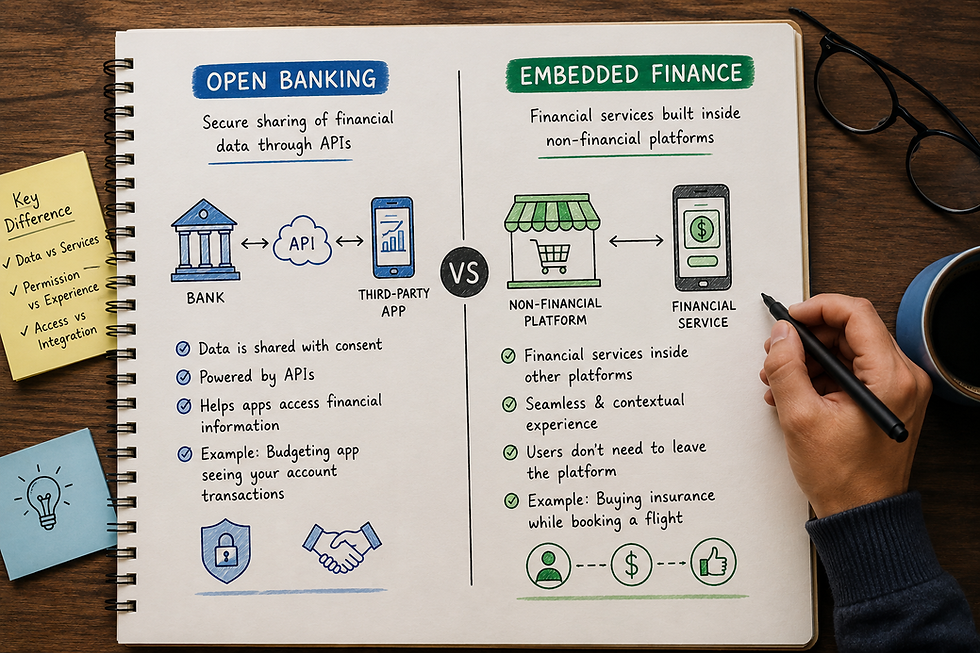

5. Embedded Lending Experiences

Modern borrowers expect lending to be integrated directly within apps:

E-commerce platforms offering BNPL

Ride-hailing apps offering driver loans

Payroll platforms offering salary advances

Investment apps offering margin financing

This is possible only when you have a flexible, API-first fintech loan management technology infrastructure.

6. Smarter Collections & NPA Management

In both India and the US, collection efficiency directly impacts profitability. A next-gen loan automation system includes:

Dynamic repayment reminders

Auto-bucket movement

Soft collections workflows

NPA prediction models

Rule-based escalation

Integration with recovery partners

This improves recovery and reduces default rates significantly.

7. Unified Dashboard With Real-Time Analytics

A modern LMS for digital lending provides real-time visibility across:

Borrower performance

Revenue metrics

NPA percentage

Risk exposure

Operational efficiency

Collection health

Compliance alerts

This allows lenders to make informed and timely business decisions.

8. Localization for India and the US

FintegrationFS specializes in building multi-region lending solutions. A modern LMS adapts seamlessly to:

India-specific needs

UPI Autopay

NACH

Mandates

Aadhaar-based onboarding

AA framework

GST & KYB workflows

US-specific needs

ACH payments

Credit bureau standards

OFAC/AML

Social Security verification

Tax document handling

This dual readiness is essential for fintechs targeting international growth.

Why Lenders Are Choosing FintegrationFS

FintegrationFS builds custom LMS platforms tailored for:

Digital lenders

NBFCs

Microfinancing companies

Credit unions

Neobanks

BNPL companies

Lending startups

Embedded finance platforms

Instead of giving you a one-size-fits-all tool, we build a modern, API-driven, secure, scalable LMS designed around your workflows.

FAQ

1. What is a modern loan management system and why is it important today?

A modern loan management system is an end-to-end digital platform that automates everything from customer onboarding and underwriting to collections and reporting. It’s important today because customers expect fast approvals, lenders need real-time compliance, and competition in digital lending is increasing rapidly. A modern LMS helps lenders operate more efficiently, reduce risk, and scale with confidence.

2. How does an LMS improve the digital lending experience in India and the US?

In India, an LMS integrates Aadhaar, PAN, DigiLocker, and account aggregator flows to offer instant verification. In the US, it connects with SSN verification, OFAC checks, credit bureaus, and ACH processors. Together, a loan management system ensures faster onboarding, error-free compliance, and a seamless digital lending experience for borrowers across both markets.

3. Can a loan management system help reduce loan defaults?

Absolutely. With AI-driven underwriting, real-time borrower monitoring, and automated reminders, a modern loan management system helps lenders identify risks early and take timely action. Smart workflows also guide borrowers through payments, reducing delays and improving overall repayment rates.

4. Is a cloud-based loan management system secure for sensitive financial data?

Yes. A cloud-based loan management system follows strict security standards like data encryption, multi-layer access control, SOC2, GDPR, and RBI/FDIC-aligned frameworks. Cloud environments also offer high availability and disaster recovery, making them safer than outdated on-prem systems.

5. Can FintegrationFS custom-build a loan management solution for my fintech or NBFC?

Yes. FintegrationFS specializes in building fully customized LMS platforms tailored to your underwriting logic, workflows, compliance rules, payment methods, and market (India or USA). If you're scaling or planning to launch a new lending product, a personalized loan management system ensures faster execution and stronger long-term performance.