Why Fintech Startups Prefer Custom Loan Management Systems Over Off-the-Shelf Tools

- Arpan Desai

- Dec 11, 2025

- 4 min read

Updated: Jul 3

Fintech startups prefer custom loan management systems over off-the-shelf tools because they offer scalable workflows, seamless API integrations, AI-driven credit scoring, automated underwriting, and real-time compliance monitoring. Unlike generic platforms, custom LMS solutions allow lenders to optimize loan processing, reduce errors, and deliver personalized borrower experiences while scaling efficiently in the US fintech market. |

1. Introduction: The Rise of Custom Loan Management Systems

In 2026, fintech startups across the USA are rapidly shifting from traditional off-the-shelf loan software to custom loan management systems. The reason is simple: off-the-shelf tools are rigid, generic, and often fail to scale with unique startup needs.

Startups adopting custom LMS solutions report 50% faster loan approvals and 40% fewer errors, giving them a competitive edge in a market where speed, compliance, and efficiency are everything.

If you want to explore modern, scalable solutions, check out FintegrationFS Loan Management System.

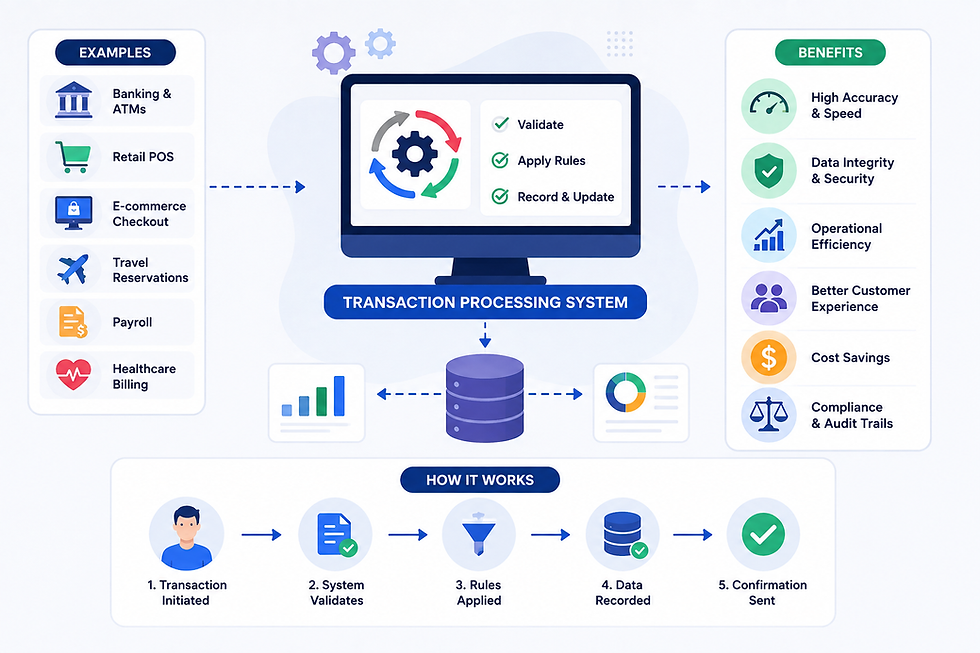

2. What is a Loan Management System (LMS)?

A loan management system is software that manages the full lifecycle of a loan: origination, servicing, and collection.

Core functions include:

Loan origination and application management

Borrower onboarding and verification

Payment processing and tracking

Compliance and reporting

Why choose a custom LMS vs off-the-shelf?

A custom LMS is fully adaptable to your product workflows, integrates easily with fintech APIs, and scales with your business, unlike generic platforms.

3. Limitations of Off-the-Shelf Loan Management Tools

Many startups try to use generic LMS software but quickly encounter issues:

Workflows that don’t match unique lending products

Difficulty in scaling or customizing features

Limited integration with online loan management systems, loan monitoring systems, or banking APIs like Plaid and Codat

Lack of AI or advanced analytics for risk assessment

Potential compliance gaps for US regulations like FCRA and ECOA

4. Advantages of Custom Loan Management Systems for Startups

Custom LMS solutions offer distinct advantages:

Fully tailored workflows for your lending products

Seamless integration with banking APIs, credit bureaus, and fintech services

AI-driven credit scoring, fraud detection, and loan optimization

Scalable architecture to grow with your user base

Faster decision-making and automated processing

Real-time dashboards for reporting and analytics

Check FintegrationFS for enterprise-grade solutions.

Transform your lending workflow with a custom loan management system designed for fintech startups. Automate loan origination, compliance, and portfolio monitoring while scaling your operations seamlessly. Don’t let generic tools hold back your growth—build a system that grows with your business.

5. Key Features Startups Include in Custom LMS

Borrower onboarding & KYC integration

Loan origination with automated underwriting

AI-powered risk and credit scoring

Payment scheduling and auto-collection

Compliance and regulatory monitoring

Loan portfolio analytics and reporting

Workflow automation (approvals, notifications, reminders)

Integration with payment processors and banking APIs

6. Benefits for Fintech Startups

Operational Benefits

Reduced manual work

Faster loan processing

Lower operational costs

Strategic Benefits

Flexibility to launch new loan products

Competitive advantage in the market

Ability to scale rapidly with custom features

User Experience Benefits

Transparent loan tracking

Personalized borrower offers

Faster approvals and disbursement

7. Use Cases in the US Fintech Market

Consumer lending platforms

Small business lending

Mortgage and personal loans

Fintech marketplaces offering embedded loans

Alternative lending platforms using AI and automation

8. Future Trends in Custom Loan Management Systems

AI-driven underwriting and decisioning

Cloud-native LMS for scalability and security

Integration with open banking APIs

Embedded finance and real-time credit scoring

Continuous learning systems to improve risk management

9. Implementation Considerations

Budget and development timeline for custom LMS

Compliance with US lending regulations (FCRA, ECOA)

Integration with existing fintech infrastructure

Data privacy, encryption, and cybersecurity requirements

10. Conclusion

Custom loan management systems empower fintech startups to innovate faster, scale efficiently, and provide superior borrower experiences compared to off-the-shelf tools.

A custom loan management system allows fintech startups to automate loan origination, servicing, and compliance, integrate with APIs like Plaid and Codat, and leverage AI for faster approvals and risk assessment.

Explore how FintegrationFS builds secure, scalable, AI-powered loan management solutions for fintech startups in the USA.

Ready to reduce manual errors and accelerate loan approvals? Explore how a custom loan management system can optimize your fintech operations, integrate with APIs, and deliver faster, smarter lending experiences to your customers.

FAQs

What is a custom loan management system?

Software tailored to manage loan origination, servicing, and collection with automation and AI.

Why do fintech startups prefer custom LMS over off-the-shelf?

Custom LMS offers scalable workflows, API integrations, compliance, and advanced analytics.

Can a custom LMS integrate with banking APIs?

Yes. Integrations include Plaid, Codat, payment gateways, and credit bureau APIs.

What features are essential in a custom LMS?

Borrower onboarding, automated underwriting, AI credit scoring, payment tracking, and compliance monitoring.

How does AI improve a custom LMS?

AI enables faster credit assessment, fraud detection, loan optimization, and predictive repayment insights.

Is a custom LMS compliant with US regulations?

Yes. It can be built to follow FCRA, ECOA, and other state/federal lending laws.

What are the operational benefits of custom LMS?

Reduced manual processing, faster loan approvals, lower operational costs, and error reduction.

Can custom LMS scale with my fintech startup?

Absolutely. Cloud-native architecture allows rapid scaling for increasing borrowers and products.

What is the typical implementation timeline?

An MVP may take 8–12 weeks; enterprise-grade solutions with AI and full compliance can take 4–6 months.

Why choose FintegrationFS for custom LMS development?

Because we build secure, AI-powered, scalable loan management systems tailored for US fintech startups.