Plaid Integration Services for FinTech Apps in the USA: What Founders Should Know Before Building

- Arpan Desai

- Jun 2

- 9 min read

Updated: Jul 6

Table of Content:

Plaid integration services help FinTech startups in the USA securely connect bank accounts, verify users, and enable real-time financial data access. Before building, founders should evaluate API capabilities, compliance, scalability, security, and integration costs to create a reliable, user-friendly financial application. |

Look, building a fintech app is thrilling. You've got a killer idea, passionate investors, and a vision to disrupt the financial industry. But here's where things get real: connecting your app to actual bank accounts is a whole different beast.

This is where Plaid integration services come in. And if you're serious about building something that works at scale in the USA, understanding Plaid isn't optional—it's essential.

Let me walk you through everything you need to know before diving into this integration.

What Are Plaid Integration Services, Really?

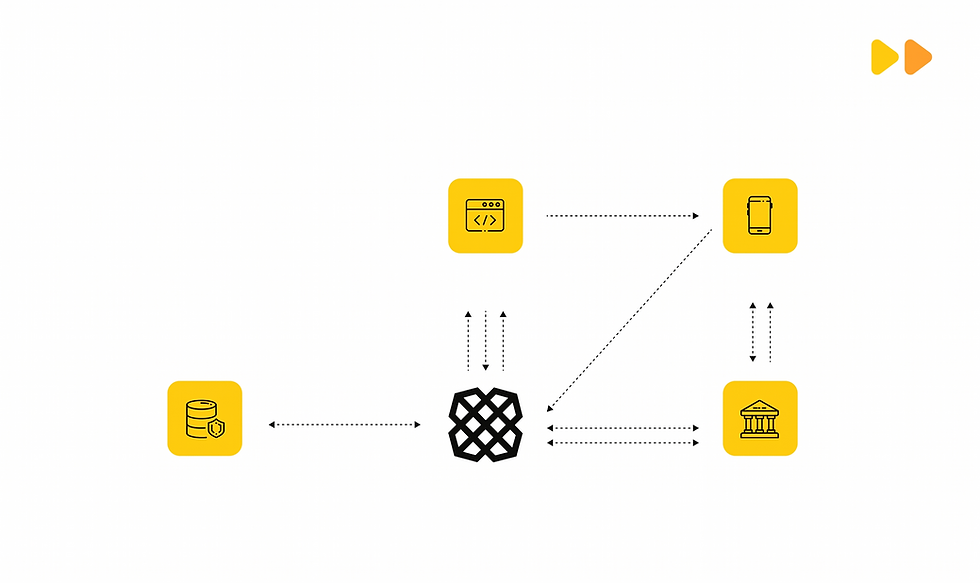

Plaid integration services aren't just a fancy API you bolt onto your app and call it a day. Think of it more like the nervous system connecting your fintech app to thousands of financial institutions across the USA.

Plaid acts as a secure bridge between your application and users' bank accounts. It handles the messy part—the part that gives you nightmares—which is safely connecting to hundreds of different banks with their own authentication systems, data formats, and quirks.

Here's what plaid integrations typically handle:

Bank account linking - Users connect their accounts securely

Transaction data access - Pull historical spending data

Account verification - Confirm routing and account numbers

Identity verification - Verify who users actually are

Balance checks - Real-time or cached balance data

Income verification - For lending products

ACH payment support - Move money between accounts

Investment and liability data - For comprehensive financial apps

But here's the thing: it's not plug-and-play. Even if you're working with experienced plaid developers, you'll need proper backend setup, security architecture, consent flows, webhook handling, and legitimate product logic. It's the iceberg situation—what looks simple on the surface has serious complexity underneath.

Why Plaid Matters for FinTech Apps in the USA

The USA fintech ecosystem runs on Plaid. Seriously. If you're building a personal finance app, lending platform, neobanking solution, or investment tool in the USA, your users expect seamless bank connectivity.

Without Plaid (or similar services), you're asking users to share their banking credentials directly with your app. That's 2005-level security thinking, and modern users—rightfully—don't trust it. Plaid lets you respect user security while getting the financial data you need.

The barrier to entry for fintech founders has dropped dramatically because of services like this. You don't need to negotiate directly with Chase, Bank of America, and 5,000 credit unions individually. Plaid does that heavy lifting.

Whether you're targeting:

Personal finance and budgeting

Lending platforms

Neobanking solutions

Wealth and investment platforms

Accounting software

Payment apps

Financial wellness platforms

Plaid is probably in your critical path.

What Founders Should Know Before Choosing Plaid

Before you commit to plaid integrations, answer these business questions (not the technical ones):

What data do you actually need?

Don't fall into the "we'll use everything" trap. Each data point requires additional security, compliance work, and storage considerations.

One-time access or continuous syncing?

Pulling transactions once is very different from maintaining a real-time sync of a user's financial life.

Which Plaid products serve your core value?

Are you verifying accounts, analyzing spending, facilitating payments, or assessing creditworthiness? Different problems, different products.

How will you explain this to users?

"We connect to your bank" is vague. Users are nervous about sharing financial data. You need a clear, honest narrative.

What's your fallback plan?

Banks go down, Plaid has occasional issues, users forget passwords. What happens then?

The founders who struggle with Plaid integration aren't struggling with technology—they're struggling because they didn't clearly define what financial data their product actually needs.

Common Plaid Products Used in FinTech Apps

Here's a quick reference for where different plaid developer tools fit:

Plaid Product | Best Used For |

Plaid Link | User bank account connection and onboarding |

Auth | Account and routing number verification |

Transactions | Spending history and cash flow analysis |

Identity | User identity verification and KYC |

Balance | Real-time or cached balance checks |

Assets | Lending and underwriting workflows |

Income | Income verification for lending |

Transfer | ACH money movement between accounts |

Investments | Wealth and portfolio tracking |

Liabilities | Loan, credit card, and debt insights |

Most fintech products use 2-4 of these. Trying to use all 10? That's scope creep talking.

Why Backend Architecture Matters (More Than You'd Think)

Here's where many founders go wrong: they treat Plaid like a frontend problem. "We'll just add Plaid Link to our app!" they say confidently.

Then reality hits.

Plaid should never be handled only from your frontend. Period.

Your backend needs to handle:

Exchanging public tokens securely - Plaid gives you temporary tokens from the frontend; your backend converts these to permanent access tokens

Storing access tokens safely - This is sensitive, requires encryption, and audit trails

Managing API requests efficiently - Rate limiting, queuing, error retries

Handling user sessions - Mapping Plaid accounts to your users

Protecting financial data - Encryption at rest and in transit

Creating audit logs - Compliance demands you track who accessed what and when

Structuring your database - Designing tables to handle transaction history, account metadata, and sync status

Connecting Plaid data to business logic - Transaction categorization, spending insights, lending decisions

This is where hiring experienced Plaid developers makes sense. They've seen the edge cases and pitfalls.

Security and Compliance Considerations

You're literally handling people's banking credentials and financial data. The stakes are high.

Think about:

User consent - Clear, explicit permission for each data type

Data minimization - Only request what you actually need

Encryption - Both in transit and at rest

Secure token storage - Never log credentials or access tokens

Role-based access - Not every team member needs every database table

Audit trails - Track all data access for compliance investigations

Privacy policy updates - Be honest about what you collect and why

Data retention rules - When do you delete transaction history?

Vendor risk review - Understand Plaid's security certifications and track record

For anything regulated (lending, wealth management), work closely with legal and compliance advisors. Financial regulations are no joke, and the costs of getting this wrong are substantial.

User Experience Matters More Than Founders Think

Bank linking is one of the most sensitive moments in your fintech journey. Users are naturally suspicious. "Why do you need my bank connection?" is a legitimate question.

Make the flow trustworthy:

Explain why you need bank access before asking for it

Keep onboarding simple—fewer screens, clear language

Use error messages that help users recover, not confuse them

Give users control—show connected accounts, allow disconnections

Support reconnect flows when credentials expire

Avoid asking for unnecessary data

Use recognizable branding and secure language

Test the flow yourself on Plaid's sandbox environment first

The difference between a fintech app that retains 70% of users post-signup and one that loses half? Often it's the bank-linking experience.

Webhooks, Errors, and Real-World Edge Cases

Here's what separates amateurs from professionals: understanding that plaid integrations don't end after the first successful connection.

Your system needs to handle:

Bank login failures - Wrong password entered by user

MFA issues - Multifactor authentication breaking your sync

Expired credentials - Users changed their password, your token is now invalid

Institution downtime - Chase's servers are unreachable for 2 hours

Duplicate accounts - User linked the same checking account twice

Delayed transactions - That Starbucks charge shows up 3 days later

Removed accounts - User disconnected their account directly in their bank's app

Webhook failures - Your server was down when Plaid tried to notify you

Re-authentication needs - Some banks require periodic re-verification

This is exactly why experienced plaid developers and integration services are valuable. They've built the retry logic, error handling, and recovery flows that make the system resilient.

Cost Factors in Plaid Integration

Let's talk money. Plaid charges per transaction or per user (pricing model varies), but the total cost of ownership for Plaid integration includes:

Number of Plaid products used - More products = higher fees

Web vs. mobile - Different pricing tiers

Backend complexity - More complex architecture takes more engineering time

Data processing requirements - Transaction volume affects costs

Dashboard and reporting needs - Additional features add up

Compliance requirements - Audit-ready systems cost more to build

Testing and QA - Proper testing prevents expensive production issues

Ongoing maintenance - Keeping up with API changes and bank updates

Most startups underestimate the true cost of integration. It's not just the Plaid subscription—it's the engineering effort to do it right.

Mistakes Founders Should Avoid

Learn from others' mistakes (so you don't repeat them):

Treating Plaid as a simple API task - It's not. It's a foundational architectural decision.

Not planning data storage properly - Transaction volume grows faster than you expect.

Ignoring webhook handling - Async events will bite you without proper architecture.

Asking for too much user data - Scope creep creates security and compliance nightmares.

Poor error handling - Users will encounter edge cases your team didn't anticipate.

No sandbox testing - Test thoroughly before production. Plaid offers sandbox for a reason.

Weak security practices - You're handling financial data. This isn't a social app.

No maintenance plan - Banks update their systems. Plaid updates their APIs. You need to keep up.

No mapping between Plaid data and product value - Why are you collecting this data? How does it serve users?

How to Choose the Right Plaid Integration Partner

If you're bringing in external help (and many founders should), look for:

Fintech product experience - Have they built similar products before?

Plaid API expertise - Do they understand the nuances and limitations?

Backend and security knowledge - Can they build resilient, secure systems?

Understanding of financial workflows - Lending, accounting, payments—each has different requirements

Experience with specific use cases - ACH payments, lending, accounting—different workflows

Scalable architecture - Will their solution grow with you?

QA and testing processes - How do they validate Plaid integrations?

Ongoing support capability - Can they help maintain and update the integration?

This is worth vetting carefully. A bad integration decision early cascades into months of refactoring work.

When Should You Use Plaid Integration Services?

Consider professional help when building:

A fintech MVP that needs to work quickly

A lending platform (compliance complexity is real)

A bank-linked personal finance app

A payment or ACH product

Bookkeeping or accounting software

Wealth management solutions

A financial wellness platform

Any product handling sensitive financial data

Basically: if Plaid is core to your product, and your timeline is tight, working with experienced teams makes economic sense.

Final Thoughts

Plaid integration services have democratized fintech. But that democratization comes with responsibility. You're handling people's financial data, and users trust you with that.

The technical implementation matters, sure. But the foundations matter more: clear thinking about what data you actually need, proper security architecture, honest user communication, and realistic timelines.

The fintech founders winning right now? They're not the ones trying to do everything themselves. They're the ones who understand their product deeply, partner with teams who understand Plaid deeply, and build systems that respect user security while delivering value.

If you're serious about building fintech in the USA, start with these questions, not the code. Get the architecture right first. Then worry about the implementation.

And if you need help navigating plaid integrations or want to work with experienced teams, we're here to help build it right.

Ready to build your fintech integration? Explore Plaid integration services or hire experienced Plaid developers who understand the USA fintech landscape.

FAQ

1. What are Plaid integration services?

Plaid integration services help fintech apps connect with Plaid APIs so users can securely link their bank accounts. These services usually include Plaid Link setup, backend API integration, token handling, transaction data sync, account verification, webhook setup, testing, and ongoing support.

2. Why do fintech apps in the USA use Plaid?

Fintech apps in the USA use Plaid because it helps users connect their bank accounts safely and quickly. It can support use cases like personal finance tracking, lending, ACH payments, income verification, balance checks, investment data, and financial wellness tools.

3. Is Plaid integration only needed for bank account linking?

No. Bank account linking is only one part of Plaid. Depending on your fintech product, Plaid can also help with transaction history, identity data, account verification, income checks, balance data, investment accounts, liabilities, and ACH-related workflows.

4. What should founders know before starting Plaid integration?

Founders should first understand what financial data their app actually needs. They should also plan the user consent flow, backend security, data storage, webhook handling, error management, and compliance requirements. A good Plaid integration is not just technical, it also affects user trust and product experience.

5. How long does it take to integrate Plaid into a fintech app?

The timeline depends on the app’s complexity. A basic Plaid Link and account verification setup can be faster, while transaction analytics, lending workflows, ACH payments, dashboards, and compliance-heavy use cases may take longer. The best approach is to define the exact use case before estimating the timeline.

6. What mistakes should founders avoid with Plaid integration?

Common mistakes include treating Plaid as a simple API task, storing tokens carelessly, not handling webhooks, asking users for unnecessary data, skipping sandbox testing, ignoring failed bank connections, and not planning for future maintenance. These mistakes can hurt both security and user experience.

7. Why work with an experienced team for Plaid integration services?

An experienced team can help you build the integration correctly from day one. They understand Plaid APIs, fintech workflows, backend security, user consent, testing, and real-world edge cases. This helps founders launch faster, reduce risk, and create a smoother experience for users.