Best Practices for Plaid API Security and Compliance in US Fintech Apps

- Arpan Desai

- 2 days ago

- 7 min read

Table of Content:

If you're building a fintech app in the US, you've probably heard the phrase "Plaid API security compliance USA" more times than you'd like. And for good reason.

Your users are trusting you with their bank accounts, account numbers, and transaction histories. That's not something to take lightly—and that's definitely not something to mess up.

Here's the truth: Plaid makes bank connectivity easier. But Plaid API security and compliance still depends heavily on how your app is designed, built, monitored, and maintained. Think of Plaid as providing the tools. Your team builds the fortress.

In my 10 years working with fintech companies across the US market, I've seen teams get this right—and I've watched others learn the hard way. This guide walks you through the exact practices that separate secure, compliant fintech apps from the ones that end up in headlines for the wrong reasons.

Plaid's Role vs. Your App's Responsibility

Let's be clear upfront. Plaid's role as a fintech API provider is to handle secure bank connectivity, tokenized access, and data APIs. But your app's role—the part that keeps you awake at night—is user consent, token storage, access control, logging, monitoring, and responsible data usage.

Your payment processor or banking partner handles the actual money movement. You handle everything else. It's a three-layer sandwich, and you're responsible for making sure the middle layer doesn't fall apart.

The good news? If you're working with a plaid developer or have access to solid plaid developer tools, the framework is already there. You just need to implement it correctly.

Start with User Consent—Make It Crystal Clear

Before a single line of code hits production, your users need to understand what data you're accessing and why.

I've audited consent screens that read like legal documents from 1987. Don't do that. Your users shouldn't need a law degree to understand what they're agreeing to. Here's what works:

Show exactly what you're accessing. "We'll see your last 30 days of transactions to categorize your spending" beats "We may access account data."

Explain the why. Users accept security better when they understand the business reason. Budget tracking? Fraud detection? Loan qualification? Say it.

Avoid collecting unnecessary data. If you only need account verification, don't request transaction history just because Plaid's API offers it. This is the principle of least privilege in action.

Give control. Let users disconnect linked accounts anytime. This builds trust and reduces your compliance headaches.

Simple, transparent consent isn't just good security—it's table stakes for US fintech apps in 2026.

Token Security: Your First Line of Defense

Let me be direct: token handling is where most fintech security issues actually happen. Not at Plaid's end. At yours.

Here are the non-negotiables:

Never expose access tokens on the frontend. Not in JavaScript. Not in localStorage. Not in Redux state that someone with browser DevTools can inspect. Ever.

Store tokens securely on the backend. That means encrypted at rest, encrypted in transit (always HTTPS), and stored in a database where not every developer can casually query them. Consider a dedicated secrets management system like HashiCorp Vault or AWS Secrets Manager.

Rotate secrets regularly. This isn't optional theater. If a developer leaves, rotate. If there's a hint of exposure, rotate. Make it part of your operations routine.

Limit developer access to production credentials. Your junior dev doesn't need to decrypt production tokens. Your CTO probably doesn't either. Implement role-based access from day one.

Separate sandboxes, development, and production environments completely. Your plaid developer account should have environment-specific credentials. Test with Plaid's sandbox. Never, ever use real customer data for testing.

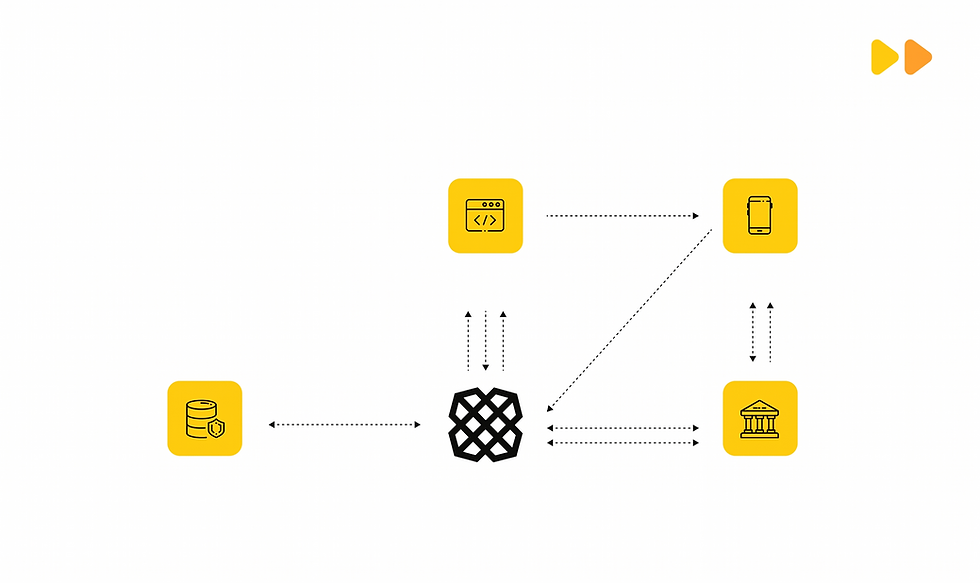

Build Strong Backend Architecture

Your Plaid integration should never live on the client side. Period.

All API calls to Plaid? Backend. All token exchanges? Backend. All sensitive data processing? Backend.

Here's the architecture that works:

Frontend: User initiates a connection (via Plaid Link). Plaid returns a public token.

Backend: Your server exchanges that public token for an access token. You encrypt and store the access token.

Data flows: Whenever you need data, your backend calls Plaid APIs using the stored token.

Frontend: Receives only the data your backend decides to send—nothing more.

Your backend should also handle input validation, rate limiting, comprehensive request logging, and error messages that don't accidentally leak sensitive details. "Invalid request" beats "Invalid token for account 123456" every single time.

Access Control: Not Everyone Gets the Keys

This is where fintech teams often stumble. Someone gives a support team member access to "see what's wrong," and suddenly they're viewing raw customer bank data.

Don't do that. Define clear roles:

Support team: Can see limited account status ("Account connected," "Last verified 3 days ago")

Compliance team: Can access audit logs and aggregated security metrics

Developers: Cannot access raw production data by default. They get staging and sandbox.

Admins: Can do anything, but every action is logged

Role-based access control (RBAC) isn't just a nice-to-have. It's essential for Plaid API security and compliance in the US fintech market, where regulators and auditors are specifically looking for this.

Audit Logs: Document Everything

When money and trust are involved, "we don't know what happened" is not an acceptable answer.

Audit logs should track:

Who accessed which customer data

When they accessed it

Why they accessed it (or at least which system/API call initiated it)

What happened as a result

Any failures or errors

These logs become your defense during security reviews, compliance audits, customer disputes, and—hopefully never—investigations.

Secure Webhook Handling

Plaid webhooks are how your app stays in sync with bank data. But they're also a potential attack surface if handled carelessly.

Verify webhook authenticity. Plaid signs webhooks. Verify the signature. Don't just process webhooks from random internet requests.

Use HTTPS endpoints only. This should go without saying, but I've seen apps mess this up.

Design for idempotency. Webhooks can retry. Your webhook handler should be smart enough to process the same webhook twice without creating duplicate records.

Monitor failed webhooks. A sudden spike in webhook failures could mean your service has a problem or a bank has an issue. Either way, you need to know.

Data: Encryption, Retention, and Deletion

Fintech apps shouldn't hoard data. Define clear retention policies:

How long do you actually need to keep transaction history?

What data gets deleted when a user closes their account?

When do you disconnect inactive bank accounts?

And whatever you keep should be encrypted at rest, in transit, backed up securely, and accessible only to systems that actually need to decrypt it. Monitor access patterns for unusual activity.

Environment Separation: Test Smart, Not with Real Data

Use Plaid's sandbox for testing. This is non-negotiable.

Never test production workflows with real customer data. Create synthetic data.

Mask sensitive fields in staging environments. Keep production credentials restricted to the absolute minimum number of systems and people.

This separation is where security meets operational efficiency.

Compliance in the US Fintech Market

Compliance isn't paperwork. It's architecture.

Depending on your business model, you might need to consider:

Privacy regulations (state-level CCPA-like laws, FTC standards)

Banking partner requirements (your bank has specific security demands)

SOC 2 readiness (many institutional customers require it)

NACHA rules (if you're moving ACH payments)

Vendor due diligence (if you're selling to regulated institutions)

These requirements should influence your product design, data access policies, monitoring strategy, and support workflows. They're not afterthoughts—they're foundational.

Building Your Security Roadmap

Here's a practical sequence that works:

Define your exact Plaid use case. Account verification? Transaction data? Payment initiation?

Map required data and products. Only request what you need.

Design the consent flow. Make it transparent.

Build secure backend token handling. Non-negotiable.

Add access control and audit logs. Know who sees what.

Test thoroughly in Sandbox. Plaid's plaid developer tools are built for this.

Review compliance requirements specific to your business and geography.

Launch with monitoring. Track API health, connection failures, unusual patterns.

Improve based on real behavior. Security is iterative.

The Common Mistakes You'll Want to Avoid

After a decade in this space, here are the ones I see repeatedly:

Storing tokens insecurely (or worse, in plain text)

Exposing secrets in frontend code or GitHub repositories

Requesting way more data than you actually use

Weak webhook handling and signature verification

Error messages that accidentally leak sensitive information

Zero audit logging

Treating compliance as paperwork instead of product design

Launching without production monitoring

Assuming Plaid handles everything (they don't)

Continuous Monitoring After Launch

Security doesn't end at launch. It's ongoing.

Monitor:

API error rates and patterns

Bank connection health metrics

Failed account verification events

Unusual access patterns or data requests

Webhook failure trends

User complaints related to security or data access

A plaid developer or dedicated API team should review these metrics weekly.

Final Thoughts

Plaid API integration isn't just a technical feature. It's a trust layer inside your fintech app.

When security and compliance are planned from the beginning—not bolted on later—fintech companies can build smoother user experiences, reduce regulatory friction, and create a foundation for long-term growth.

Your users are trusting you with their financial lives. Plaid API security and compliance means you earned it.

FAQ

1. Why is Plaid API security important for US fintech apps?

Plaid API security is important because fintech apps handle sensitive financial data such as bank account details, balances, transactions, identity information, and payment-related workflows. A secure Plaid integration helps protect user trust, reduce data risk, and support compliance expectations in the US fintech market.

2. What are the best practices for Plaid API security and compliance?

The best practices include secure token storage, backend-only API calls, encrypted data handling, clear user consent, role-based access control, webhook verification, audit logs, environment separation, and continuous monitoring. The goal is to make security part of the product design, not something added after launch.

3. Should Plaid access tokens be stored on the frontend?

No, Plaid access tokens should never be stored or exposed on the frontend. They should be stored securely on the backend using encryption and strict access controls. Exposing tokens in a browser, mobile app, or public repository can create serious security risks.

4. How can fintech apps handle user consent properly with Plaid?

Fintech apps should clearly explain why they need bank data, what information will be accessed, and how it will be used. Users should not feel confused during the linking process. Simple consent language, transparent privacy communication, and easy account disconnection options can improve trust.

5. How do Plaid webhooks affect security and compliance?

Plaid webhooks help fintech apps receive important account and data updates, but they must be handled securely. Apps should use HTTPS endpoints, verify webhook events, avoid logging sensitive data, process retries properly, and monitor failed webhook events. Poor webhook handling can lead to data gaps or operational issues.

6. What mistakes should fintech teams avoid during Plaid API integration?

Common mistakes include exposing API secrets, storing tokens insecurely, requesting more data than needed, skipping audit logs, using weak access controls, ignoring webhook failures, testing with real user data unnecessarily, and treating compliance as a last-minute checklist.