How to Integrate Plaid ACH Payments Into Your US Lending Platform

- Arpan Desai

- 3 days ago

- 12 min read

Table of Content:

Lending is stressful enough for borrowers without making the payment experience worse. Yet somehow, many lending platforms still ask borrowers to manually enter routing numbers, account numbers, and hope they got it right. Spoiler alert: they usually don't.

That's where Plaid ACH payment integration comes in. When implemented correctly, it transforms the payment experience from "fill out this form and hope" to "securely connect your bank account in two taps."

If you're building or scaling a US lending platform, understanding how to integrate Plaid for ACH payments isn't optional—it's becoming table stakes. And yes, this guide will walk you through exactly how to do it.

What Is Plaid ACH Payment Integration, Really?

Here's the thing about Plaid: it's not just a "connect your bank" button, even though that's what borrowers see.

On the surface, Plaid integrations give borrowers an easy way to securely connect their bank accounts to your lending platform. Behind the scenes, Plaid is handling bank verification, collecting account details, and enabling safe ACH payment workflows. The magic happens when you combine Plaid's account verification capabilities with a payment processor partner to actually move money.

Think of it this way: Plaid gets your borrowers' bank information verified and secure. Your payment processor (or banking partner) moves the actual dollars. Plaid enables the connection; your lending platform controls the experience.

Why US Lending Platforms Are Moving to Plaid for ACH Payments

Here's what happens when borrowers manually enter their bank details:

Failed payments because someone transposed a digit

Support tickets asking "Why did my payment fail?"

Manual verification headaches for your operations team

Slower onboarding because you need to verify everything twice

Borrower frustration that leads to abandoned loan applications

When you implement Plaid developer tools properly, all of that friction disappears.

Lending platforms use Plaid ACH payment integration because it delivers:

Bank account verification that's actually accurate

Faster borrower onboarding (borrowers connect bank accounts in 90 seconds instead of 10 minutes)

Fewer failed payments because account details are verified at connection time

Better borrower experience that feels modern and secure

Cleaner financial data for reconciliation and reporting

Nobody wants their borrowers typing routing numbers and hoping they got it right. Plaid solved that problem, and now most competitive US lending platforms use it.

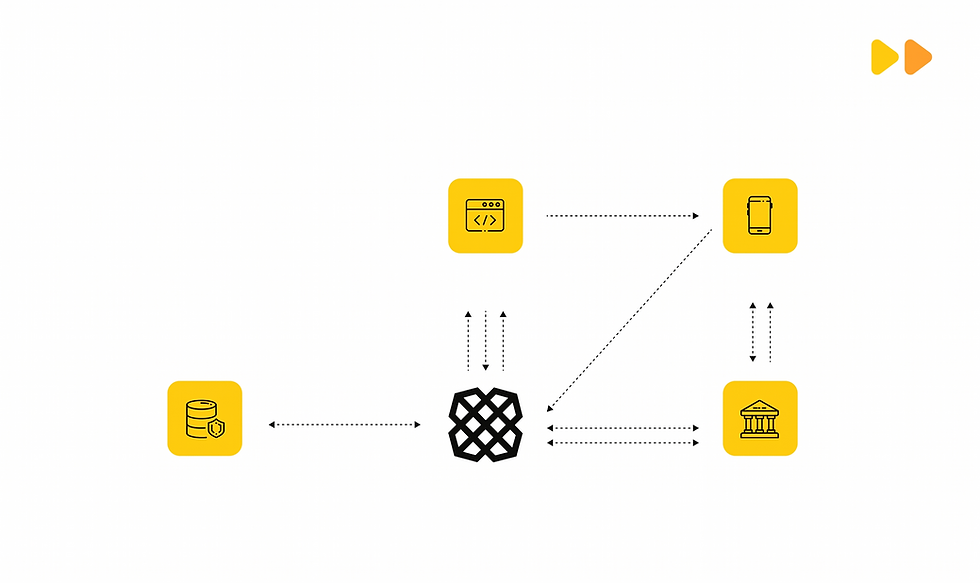

Where Plaid Fits in Your Lending Payment Flow

Understanding the full picture matters. Plaid doesn't handle everything, and that's actually a feature, not a bug.

Here's the typical flow when Plaid ACH payment integration is done right:

Step 1: Borrower Application Borrower starts their loan application on your platform. Standard stuff—income, employment, loan amount.

Step 2: Bank Connection (Plaid) When it's time to set up repayment, borrower sees a button to "Connect Your Bank Account." Behind the scenes, this opens Plaid Link. Borrower selects their bank, logs in, and Plaid securely captures their account details.

Step 3: Account Verification (Plaid) Plaid verifies the account details with the bank. Your platform now has confirmed account and routing numbers.

Step 4: Storage and Processor Handoff Your backend stores the access token securely and passes verified account details to your ACH processor or banking partner.

Step 5: Repayment Authorization Borrower reviews repayment terms, payment amount, frequency, and authorizes the ACH debit.

Step 6: ACH Movement Your processor initiates the ACH debit from the borrower's account to your account.

Step 7: Status Tracking Webhooks keep your platform updated on payment success, failure, or pending status.

The key insight: Plaid developers build the bank connection layer; your lending platform controls the entire borrower journey. Plaid handles "get the account details securely." You handle "what happens with those details."

Key Components You Need Before Integration Starts

Before you write a single line of code, you need to plan what you're building. Here's what successful lending platforms have in place before integration:

Technical Requirements:

Plaid account and API keys (get your Plaid developer account set up first)

Lending platform backend (API to handle token exchanges and payment logic)

Plaid Link frontend component (web and mobile)

ACH processor or banking partner integration

Secure database for storing access tokens

Webhook handler for processor events

Admin dashboard for your operations team

Operational Requirements:

Clear borrower consent flow (borrowers must know what they're authorizing)

Compliance review (NACHA rules are non-negotiable)

Error handling and retry logic for failed payments

Support workflows for payment issues

Testing strategy (sandbox first, always)

A strong integration starts during planning, not during coding. Lenders who map this out properly avoid expensive rework later.

Step 1: Set Up Plaid Link for Bank Connection

Plaid Link is the user-facing component. This is what your borrowers interact with, and it should feel simple, not intimidating.

What Plaid Link Does:

Opens a secure modal or flow where borrowers select their bank

Handles bank login (Plaid manages security, not you)

Captures account details securely

Returns a public token to your frontend

Implementation Basics: On your lending platform's repayment setup page, you add the Plaid Link component. When a borrower clicks "Connect Your Bank," Plaid Link opens. They search for their bank (Chase, Bank of America, Capital One, etc.), authenticate, and Plaid captures their account information.

The borrower experience should feel like:

Click "Connect Bank"

Select your bank

Log in (to your bank, not your loan platform)

Done

No routing numbers, no account numbers, no guessing. Just a secure connection.

Mobile Considerations: Plaid Link works on web and mobile. Make sure your lending platform's mobile app has a smooth bank connection flow. Many borrowers apply and repay from their phone, so this matters.

Step 2: Exchange the Public Token for an Access Token

Here's where security becomes serious.

When Plaid Link completes successfully, your frontend receives a public token. This token is temporary and limited in scope. It's your borrower's proof that they've connected their bank, but it's not the actual account access.

Your backend must immediately exchange this public token for an access token. This happens server-to-server (your backend talking to Plaid's API), not on the borrower's phone or browser.

Why This Matters:

Public tokens expire quickly

Access tokens are long-lived and allow your backend to retrieve account details

Access tokens must be stored securely in your database

Access tokens should never be exposed to the frontend or borrower

Think of it like this: the public token is the borrower showing their ID at the bank. The access token is the key to their account that your backend holds securely.

Step 3: Verify Bank Account Details

Now that you have an access token, you can retrieve verified account information. This is one of the biggest wins of using Plaid.

What Gets Verified:

Account number (the actual, correct account number)

Routing number (also verified)

Account type (checking, savings, etc.)

Account holder name

Account status (active, closed, etc.)

Using the Plaid API (via a Plaid developer), you call the appropriate endpoint to retrieve account details. These details are verified with the bank, so you know they're accurate.

Why This Eliminates Headaches:

No more failed payments due to typos

No more "I wrote down my account number wrong" support tickets

Your ops team doesn't need to manually verify account details

You can safely proceed to ACH processor integration

Accurate bank data sounds boring, but it saves your team countless support headaches.

Step 4: Connect Plaid With Your ACH Processor

Here's an important distinction: Plaid doesn't move money.

Plaid verifies account details and secures the connection. An ACH processor or banking partner actually initiates the debit and moves the funds.

Common US ACH processors that work with Plaid:

Stripe Connect

Dwolla

Marqeta

Evolve

Green Dot

Treasury partners

Your bank's ACH API

The integration typically works like this:

You've verified account details through Plaid

Your backend passes those verified details to your ACH processor

Processor initiates the ACH debit using those account details

Processor returns a transaction ID to your platform

Your platform tracks the payment status

Some Plaid integrations are tighter with certain processors (for example, Stripe has deeper Plaid integration), while others require more manual data passing. Either way, Plaid opens the door; your processor moves the money.

Step 5: Build Borrower Consent and Repayment Authorization

Before you can debit a borrower's account, they must explicitly authorize it. This is a legal requirement under NACHA rules, not optional.

What Borrowers Must Authorize:

That you have permission to debit their account

The amount that will be debited

The frequency (one-time, weekly, monthly, etc.)

The payment schedule

Any relevant fees or terms

Best Practice Implementation: Show borrowers a clear confirmation screen that says something like:

"I authorize [Your Lending Platform] to debit my account ending in 1234 on the 15th of each month for $250 to repay my loan. I understand that if the payment fails, I may be charged a fee by my bank." |

Borrowers should have to explicitly agree (checkbox, button click, etc.). They should receive this authorization in writing (email confirmation). They should be able to review it anytime.

This isn't just legal compliance. It's also good borrower trust-building. Borrowers who know exactly when money will be debited and how much are borrowers who don't have unpleasant surprises.

Step 6: Create ACH Repayment Workflows

Now that you have verified account details and authorization, you can build the actual repayment logic.

One-Time Payments: Borrower makes a single payment toward their loan.

Scheduled Repayments: System automatically initiates ACH debits on the scheduled dates (e.g., 15th of every month).

Failed Payment Handling: If an ACH debit fails (insufficient funds, account closed, etc.), your system should:

Log the failure

Alert your support team

Retry (typically within 3-5 days)

Notify the borrower

Apply any late fees if permitted

Retry Logic: Don't give up after one failure. Smart platforms implement intelligent retry:

First attempt on scheduled date

Retry 3 days later if failed

Notify borrower before retrying

Alert support team after 2 failures

Reminders: Send borrowers payment reminders (3 days before, 1 day before, day-of) so they're not surprised by the debit.

The best repayment system works quietly in the background until something needs human attention. That's the goal here.

Step 7: Handle Webhooks and Payment Status Updates

Your lending platform should never be guessing about payment status. Webhooks tell you what actually happened.

What Events to Listen For:

Bank account successfully connected (Plaid webhook)

Bank account disconnected or invalidated

ACH payment initiated (processor webhook)

ACH payment succeeded

ACH payment failed (with reason)

ACH reversal (borrower disputes charge)

Account updated or changed

Why Webhooks Matter: Without webhooks, you might think a payment succeeded when it actually failed. Then 5 days later, a borrower calls asking why they were charged twice. With webhooks, your system knows immediately what happened.

Implementation: Your backend exposes a webhook endpoint (e.g., /webhooks/payment-status). Your processor sends real-time updates to this endpoint. Your system updates the database and takes appropriate action (mark payment complete, alert support for failed payment, etc.)

Guessing about payment status is not a lending operations strategy. Webhooks eliminate the guessing.

Step 8: Build an Admin Dashboard for Lending Operations

Your operations team shouldn't need to open five different tools just to understand one borrower's payment issue.

Essential Dashboard Views:

Borrower Profile: All linked bank accounts, current loan balance, repayment schedule

Payment History: All payments made, scheduled, and failed with dates and amounts

Linked Accounts: Currently active bank accounts, last verified date, status

Failed Payments: Why they failed, retry status, when retrying next

Pending Repayments: Upcoming scheduled payments in the next 7, 14, 30 days

Retry Status: Payments currently in retry loop, next retry date

Audit Logs: Every action taken (authorization given, payment initiated, account disconnected)

Support Actions: Ability to manually retry payments, mark payments as resolved, communicate with borrowers

Your ops team should be able to search a borrower by ID, email, or phone and see their full payment story in one dashboard.

Security Considerations for Plaid ACH Payment Integration

In lending, trust is built in small technical decisions users never see. Here's what matters:

Token Storage:

Access tokens must be encrypted in your database

Use AES-256 or similar for encryption at rest

Never log access tokens

Never expose tokens in error messages

Rotate tokens periodically (Plaid supports this)

API Security:

All Plaid API calls must happen server-to-server

Use HTTPS/TLS for all communication

Validate Plaid webhook signatures before processing

Rate-limit your API endpoints

Role-Based Access:

Operations team sees borrower payment info, not bank account numbers

Support team can see payment status, not full account details

Only senior ops staff can manually retry payments

Audit logs track who accessed what and when

Data Minimization:

Store only what you need (access token, last 4 of account number, account type)

Don't store routing numbers in plaintext

Don't store full account numbers if you can avoid it

Regularly delete old payment records per your retention policy

Secure APIs:

Require authentication for all API calls

Use API keys or OAuth tokens

Rate-limit to prevent abuse

Monitor for suspicious activity

Compliance and Borrower Transparency

Before you go live, your legal and compliance teams need to review the flow. This isn't optional.

NACHA Rules: NACHA (the organization that governs ACH) has rules about:

How and when you can debit accounts

How you must obtain authorization

What you must disclose to borrowers

Dispute procedures

Unauthorized charge limits

Data Privacy:

Borrower bank data is sensitive; handle it as such

Comply with Gramm-Leach-Bliley Act (GLBA)

Secure Socket Layer (SSL) encryption for any data in transit

Don't share borrower data with third parties without consent

Borrower Transparency:

Clear repayment disclosure before authorization

Regular statements showing payment status

Transparent failure reasons (not just "payment failed")

Easy access to view linked accounts

Simple delink mechanism if borrower wants to remove bank account

Legal Review: Have your legal team review:

Borrower authorization language

Payment disclosure statements

Failure handling procedures

Dispute procedures

Good compliance isn't just paperwork. It's being fair and clear with borrowers.

Benefits of Plaid ACH Payment Integration for US Lenders

When done right, Plaid ACH payment integration delivers real business benefits:

Faster Onboarding Borrowers connect bank accounts in 90 seconds instead of manually entering details. Loan applications move faster.

Fewer Failed Payments Verified account details mean failed payments drop dramatically (typically 50-70% reduction).

Better Borrower Experience Modern, secure bank connection feels professional. Borrowers trust platforms that integrate Plaid.

Automated Repayments Scheduled ACH debits happen automatically. Less manual work for your team. Fewer borrowers forgetting to pay.

Improved Operations Accurate data means less manual verification, fewer support tickets, cleaner reconciliation.

Cleaner Financial Data Because account details are verified, your financial records are accurate. Accounting teams love this.

Competitive Advantage Platforms without Plaid developer integrations look outdated. Borrowers expect this level of tech.

When to Hire Plaid Integration Experts

You can build this yourself, but there's a decision to make: is payment processing core to your product?

If the answer is yes—if your lending platform lives or dies on reliable repayments—hiring experts is probably smart.

You Should Hire Experts When:

Your payment flows are complex (multiple processors, custom routing, etc.)

Compliance requirements are strict (state lending licenses, etc.)

You're processing significant volume (performance and reliability matter)

You don't have Plaid developer experience on your team

You need the integration done quickly without mistakes

Fintegration connects US fintech companies with experienced Plaid developers who've built these integrations dozens of times. If your team lacks this expertise, that's worth considering.

Final Thoughts

Plaid ACH payment integration isn't complicated. It's just a series of thoughtful steps:

Borrow securely connects their bank through Plaid Link

You verify their account details through Plaid

You pass verified details to your ACH processor

Processor moves money

Webhooks keep you updated

Your team has visibility through an admin dashboard

When implemented correctly, borrowers get a frictionless experience. Your team gets reliable, automated repayments. Your operations become cleaner.

The goal is simple: make repayments easier for borrowers and more reliable for lenders.

If you're building a US lending platform and need help with Plaid ACH payment integration, let's talk to our team of experienced Plaid developers who've built this dozens of times. We can help you design the right flow, avoid common mistakes, and launch with confidence.

Or explore our Plaid integration resources and API guides to get started on your own.

FAQ

1. What is Plaid ACH payment integration for a lending platform?

Plaid ACH payment integration helps a US lending platform connect a borrower’s bank account, verify account details, and support smoother ACH repayment workflows. In simple terms, Plaid helps confirm that the borrower’s bank account is real and usable, while your payment processor handles the actual money movement.

2. Why should a US lending platform use Plaid ACH payment integration?

A US lending platform should use Plaid ACH payment integration because it reduces manual bank detail entry, improves account verification, and helps create a cleaner repayment experience. Instead of asking borrowers to type routing and account numbers manually, Plaid lets them securely connect their bank account, which can reduce errors and payment failures.

3. Does Plaid ACH payment integration move money directly?

No, Plaid ACH payment integration usually does not mean Plaid alone moves the money. Plaid helps with bank account connection and verification. The actual ACH debit or credit is typically handled through a payment processor, banking partner, or ACH provider. Think of Plaid as the secure bank connection layer, not the full payment engine.

4. How does Plaid ACH payment integration work in a loan repayment flow?

In a typical loan repayment flow, Plaid ACH payment integration starts when the borrower connects their bank account through Plaid Link. The lending platform then verifies the account, stores the required tokens securely, connects with an ACH processor, and manages repayment schedules, payment status, failed payments, and reminders through the platform.

5. Is Plaid ACH payment integration secure for borrower bank data?

Yes, Plaid ACH payment integration can be secure when implemented correctly. The lending platform should use secure token handling, encryption, role-based access, audit logs, and proper data storage practices. The key point is that security depends not only on Plaid, but also on how your development team builds the full payment workflow.

6. What are common mistakes in Plaid ACH payment integration?

Common mistakes in Plaid ACH payment integration include unclear borrower consent, weak webhook handling, poor error messages, insecure token storage, no retry logic for failed payments, and limited admin visibility. These issues can create confusion for borrowers and extra support work for lending teams.

7. When should you hire experts for Plaid ACH payment integration?

You should hire experts for Plaid ACH payment integration when your lending platform needs custom repayment schedules, ACH processor integration, borrower authorization flows, webhook handling, compliance-sensitive workflows, or production-level security. Since lending involves real money and borrower trust, this is not the best area to “figure it out later.”