Comparing the Top Loan Management Systems in India & the US (2026 Edition)

- Arpan Desai

- Dec 9, 2025

- 11 min read

Updated: Jul 2

Table of content

Lending Has Become a Technology Game — And the Stakes Are High

Let's start with a truth that every lender already knows but might not want to admit: if your loan process still involves a lot of manual steps, printed forms, and "we'll call you back in 3–5 business days," you are losing borrowers faster than you think.

In 2026, borrowers — whether in Mumbai or Minneapolis — expect faster approvals, digital documentation, real-time status updates, and flexible repayment options. The lenders winning market share are not necessarily the ones with the lowest rates. They are the ones with the smartest technology. At the center of that technology stack sits a powerful loan management solution.

This guide compares the top loan management systems across India and the US, breaks down what each market needs, and helps you figure out which direction makes the most sense for your lending operation in 2026.

What Is a Loan Management System, Really?

Before we dive into comparisons, let's make sure we are all on the same page — no jargon overload, promise.

A loan management system is software that helps banks, NBFCs, credit unions, fintechs, and lenders manage the complete loan lifecycle. We are talking everything from application and underwriting, all the way through disbursement, repayment, collections, and regulatory reporting.

Think of it as the operating system for your lending business. Without a solid one, everything else — your marketing, your customer service, your compliance — runs on borrowed time.

What Are the Top Loan Management Systems in India and the US in 2026?

The top Loan Management Systems in India and the US help lenders automate loan origination, underwriting, disbursement, repayment tracking, collections, compliance, and reporting. Leading platforms vary based on the lender’s market, loan products, regulatory requirements, integration needs, and business size.

In India, loan management platforms commonly support digital KYC, eNACH, UPI payments, credit-bureau integrations, GST data, Account Aggregators, and RBI-aligned lending workflows. In the US, systems often integrate with credit bureaus, ACH networks, open-banking providers, identity-verification tools, payment processors, and federal or state compliance solutions.

When comparing Loan Management Systems, lenders should evaluate automation capabilities, API availability, customization, scalability, data security, regulatory compliance, reporting, customer experience, implementation costs, and ongoing technical support. The best solution is one that fits the lender’s specific products and can adapt as its loan portfolio grows.

Why Loan Management Software Matters Even More in 2026

The lending landscape has shifted dramatically, and a Loan Management System comparison in 2026 looks very different from even three years ago. Here is why:

Digital lending adoption has gone mainstream across both India and the US, with borrowers now expecting app-based experiences as standard.

Borrower expectations have been permanently reset by fintech challengers who approve loans in minutes, not days.

Compliance pressure has intensified — regulators in both markets are paying close attention to digital lenders, data handling, and fair lending practices.

Automation is no longer a luxury. With growing loan portfolios and thinner margins, manual processes simply do not scale.

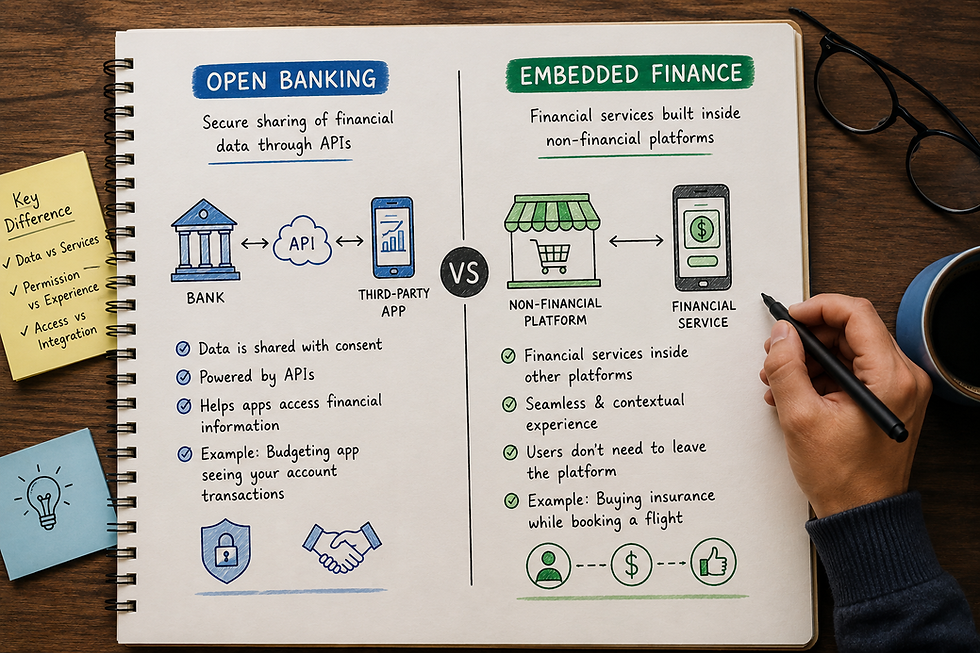

Embedded lending is exploding — financial products are appearing inside e-commerce platforms, HR tools, and SaaS products, requiring API-first loan infrastructure.

Real-time analytics are expected at the portfolio level, not just in quarterly reports.

Fintech competition has pushed traditional banks and NBFCs to modernize or lose relevance.

Key Features to Look for in a Loan Management System

Not all lending management systems are built equal. Before comparing platforms, here is what genuinely matters:

Digital loan origination — end-to-end online application flows with minimal friction

KYC/KYB and borrower verification — automated identity checks, document validation, and business verification

Credit decisioning — rule-based engines or AI-assisted underwriting to approve or decline faster

Document management — secure storage, retrieval, and e-sign capabilities

Repayment scheduling — flexible EMI structures, moratoriums, and restructuring options

EMI and instalment tracking — real-time visibility on payments due, received, and overdue

Collections workflows — automated reminders, escalation paths, and recovery management

Risk monitoring — early warning signals, portfolio health dashboards, and NPA tracking

Reporting and dashboards — regulatory reports, operational dashboards, and executive summaries

API integrations — connectivity with credit bureaus, payment rails, CRMs, and core banking systems

If a platform you are evaluating is weak on even two or three of these, that is worth pausing over.

India vs. US Lending Market: The Differences That Actually Matter

Both markets need strong loan software — but their priorities diverge significantly. Understanding this is crucial for any meaningful Loan Management System comparison in 2026.

India's lending market is defined by the explosive growth of NBFCs and digital lending apps, UPI-based repayment mandates, the Account Aggregator framework for financial data sharing, RBI compliance requirements, a large rural and semi-urban borrower base, and the need for multi-language support.

The online loan management system landscape here must handle microfinance, gold loans, MSME lending, and co-lending models — sometimes all within the same institution.

The US lending market operates around ACH-based payments, deep credit bureau integration (Equifax, Experian, TransUnion), state-level regulatory variation, a mature mortgage and auto loan ecosystem, and a growing embedded finance sector. Compliance with TILA, RESPA, ECOA, and state usury laws is non-negotiable. Borrower expectations are shaped by a highly competitive market where fintech players like SoFi, LendingClub, and Affirm have raised the bar considerably.

Different payment rails. Different compliance frameworks. Different borrower behaviors. One thing in common: both markets are unforgiving if your loan software cannot keep up.

Top Loan Management System Categories in India

India's lending ecosystem is diverse, and the loans management system landscape reflects that diversity. Here are the primary categories shaping the market in 2026:

Cloud-Based LMS Platforms for NBFCs Best fit for mid-to-large NBFCs managing retail, MSME, or vehicle loans. Key strengths include RBI-ready compliance workflows, Account Aggregator integration, and multi-product support. Potential limitations include high customization costs for niche products. Ideal for NBFCs scaling their digital lending operations.

Digital Lending Platforms Designed for app-first lenders targeting personal and consumer loans. Strengths include fast onboarding, API-native architecture, and UPI mandate support. Limitations can include weaker collections modules compared to traditional LMS platforms. Best for fintech startups and new-age digital lenders.

Microfinance Loan Systems Purpose-built for MFIs and small-ticket lending. Strong on group lending workflows, field agent apps, and vernacular language support. Can struggle with scalability if portfolio volume grows rapidly. Ideal for MFIs and rural-focused lenders.

Co-Lending Platforms Built specifically for the co-lending model between banks and NBFCs. Key strength is managing split disbursement, shared risk tracking, and regulatory reporting across two entities. Complexity in setup is a known limitation. Ideal for NBFCs with active co-lending partnerships.

SME and MSME Lending Systems Handles business loan workflows including GST data pulls, bank statement analysis, and business KYB. Strong analytical capabilities but can require significant integration effort. Best for lenders focused on the SME segment.

Gold Loan and Consumer Loan Management Tools Highly specialized for collateral-backed lending. Strengths include valuation tracking, auction management, and branch-level operations. Limited utility outside their specific loan type. Perfect for gold loan NBFCs and pawn-based lenders.

Top Loan Management System Categories in the US

The US market has its own set of well-defined loan monitoring system categories, each catering to a distinct lending segment:

Bank and Credit Union LMS Platforms Built for regulated depository institutions with enterprise-grade security, compliance controls, and core banking integrations. Strengths include deep ACH and payment rail support. Can be expensive and slow to implement. Best for community banks and credit unions.

Mortgage Loan Management Systems Highly specialized for origination, servicing, and secondary market operations. Strong on RESPA compliance, escrow management, and investor reporting. Complexity and cost are significant. Ideal for mortgage lenders and servicers.

Consumer Lending Platforms Covers personal loans, credit lines, and BNPL products. Fast deployment, strong credit bureau connectivity, and borrower-facing portals are key strengths. May lack depth for commercial loan types. Best for consumer-focused fintechs and specialty lenders.

Commercial Lending Systems Designed for business loans, lines of credit, and SBA lending. Strong on covenant tracking, financial spreading, and risk rating. Implementation timelines can be lengthy. Ideal for commercial banks and business lenders.

Auto Loan Management Systems Purpose-built for vehicle financing with dealer integration, title management, and collateral tracking built in. Excellent for auto lenders; limited outside this vertical. Best for auto finance companies and dealership finance arms.

Embedded Lending Solutions API-first platforms built for lenders operating inside other platforms — e-commerce, SaaS, payroll systems. Strengths include speed of integration, developer-friendly design, and real-time decisioning. May require more custom development. Ideal for embedded finance programs and BNPL operators.

Comparison Table: India vs. US Loan Management Systems

Category | Best For | Compliance Fit | Integration Capability |

Cloud NBFC LMS | NBFCs, mid-large lenders | RBI-ready | High |

Digital Lending Platform | Fintech, app-first lenders | RBI/FLDG rules | Very High |

Microfinance LMS | MFIs, rural lenders | RBI MFI norms | Medium |

Co-Lending Platform | Bank-NBFC partnerships | RBI co-lending | High |

SME Lending System | MSME lenders | RBI, GST | High |

Bank/Credit Union LMS | Banks, credit unions | FDIC, state laws | High |

Mortgage LMS | Mortgage lenders | RESPA, TILA | Medium-High |

Consumer Lending Platform | Fintech, personal loans | ECOA, state laws | Very High |

Commercial LMS | Business lenders | SBA, bank regs | High |

Embedded Lending | Platform lenders, BNPL | Varies by state | Very High |

Build vs. Buy: Which Option Actually Makes Sense for You?

This is the question every lender eventually faces — and there is no universal answer, which is probably not what you wanted to hear. But here is the honest breakdown.

Buy a ready-made LMS when you need to go to market quickly, your loan products are relatively standard, and you do not have the engineering resources to build and maintain custom software. Off-the-shelf platforms have come a long way and can cover 80% of use cases well.

Build a custom web based loan management system when your loan products are genuinely unique, your compliance requirements are complex and hard to configure in existing tools, you need deep integrations with proprietary systems, or you are building a platform that will serve as a competitive moat. Custom-built systems take longer and cost more upfront — but the control and flexibility they provide often justify the investment at scale.

Customize an existing platform when a commercial LMS gets you 70% there but needs tailoring for your specific market, loan type, or workflow. This hybrid approach is increasingly popular among mid-market lenders who want speed-to-market without the constraints of a purely off-the-shelf solution.

To understand the workflow implications of each approach, it helps to review how loan management software works step by step before committing to a direction.

Common Mistakes Lenders Make When Choosing an LMS

Consider this a checklist of things not to do — learned from lenders who did them anyway:

Choosing based only on price. The cheapest loan processing system is rarely the most cost-effective one. Implementation costs, customization fees, and operational inefficiencies add up quickly.

Ignoring compliance requirements. Whether it is RBI guidelines in India or state-level usury laws in the US, a platform that cannot support your regulatory environment is a liability, not an asset.

Weak API capabilities. In 2026, a loan management platform that cannot integrate cleanly with credit bureaus, payment rails, and your CRM is essentially isolated. That is a problem.

Poor borrower experience. If borrowers find the application clunky, confusing, or slow, they will abandon it. Conversion rates suffer directly.

No collections workflow. Disbursement without a solid collections module is like building a pool without a drain. At some point, it overflows.

No analytics layer. Flying blind on portfolio performance is how NPAs sneak up on you.

Not planning for scale. A system that works beautifully at 5,000 loans may buckle at 50,000. Always stress-test scalability assumptions.

Lack of payment rail integration. UPI mandates in India, ACH in the US — if your lms loan management system cannot talk to your payment infrastructure, repayments become a manual nightmare.

How AI Is Changing Loan Management Systems in 2026

Artificial intelligence has stopped being a buzzword in lending and started being a genuine operational differentiator. Here is where it is making the biggest impact in lending systems today:

AI-assisted underwriting analyses thousands of data variables — transaction history, behavioral signals, bureau data — to generate credit decisions that are faster and often more accurate than rule-based systems alone. Fraud detection models flag suspicious patterns in real time, catching synthetic identity fraud and loan stacking before disbursement. Document review automation extracts and validates data from uploaded documents in seconds, eliminating manual data entry. Collections prioritization uses predictive models to identify which accounts need immediate attention and which are likely to self-cure.

Borrower risk scoring is now dynamic — updating as borrower behavior changes through the loan term, not just at origination. Customer support automation through AI chatbots handles routine borrower queries, payment confirmations, and balance inquiries without human intervention. Portfolio performance insights give lenders a forward-looking view of their book rather than just a rearview mirror.

The lenders ignoring AI in 2026 are not being cautious — they are falling behind.

What Indian Lenders Should Prioritize in an LMS

If you are operating in the Indian market, your loan management system software selection should be guided by these priorities:

RBI-ready compliance workflows — your platform must be built with India's lending regulations as a foundation, not an add-on

Account Aggregator integration — AA-based financial data sharing is becoming standard for credit decisioning; you need native support

UPI and mandate support — repayment collection in India runs on UPI and NACH mandates; this is non-negotiable

NBFC-specific workflows — co-lending structures, FLDG arrangements, and priority sector classification all require specialized handling

Multi-language borrower communication — reaching Tier 2 and Tier 3 borrowers in their language is both a UX requirement and a competitive advantage

Branch and digital hybrid operations — many Indian lenders still operate a blend of field agents and digital channels; your LMS should support both without friction

What US Lenders Should Prioritize in an LMS

For the US market, the priorities look somewhat different:

ACH and payment integration — reliable ACH connectivity for repayments, pre-authorization, and returns management is foundational

Credit bureau connectivity — tri-merge bureau pulls, FCRA compliance, and soft-pull capabilities need to be built into the underwriting workflow

State-level compliance flexibility — with 50 different state regulatory environments, your payday loan management systems or consumer lending platform must adapt quickly to varying rate caps, disclosure requirements, and licensing rules

Bank-grade security — SOC 2 Type II, encryption at rest and in transit, and robust access controls are expected, not optional

Loan servicing automation — payment posting, escrow management, and investor reporting should run with minimal manual intervention

Embedded lending readiness — if you are building or expanding embedded finance channels, API-first architecture is essential from day one

FAQ

1. What does it mean to build a loan management system that fits your market?

It means your loan software should match your lending model, borrower behavior, compliance needs, and repayment process. A lender in India may need UPI mandates and RBI-aligned workflows, while a US lender may need ACH, credit bureau integrations, and state-level compliance flexibility.

2. Why can’t every lender use the same loan management system?

Because lending is not one-size-fits-all. A microfinance company, mortgage lender, NBFC, credit union, and fintech lender all have different workflows, risk checks, documents, approval processes, and repayment structures.

3. What features should a market-ready loan management system include?

A strong system should include digital loan applications, borrower verification, credit decisioning, document management, repayment tracking, collections workflows, payment integrations, reporting dashboards, and compliance-ready audit trails.

4. Should lenders build custom loan software or buy an existing LMS?

It depends on the business model. If your workflow is simple, an existing LMS may work. But if you have unique loan products, complex compliance needs, custom approval flows, or market-specific integrations, custom loan software can be a better long-term choice.

5. How does a loan management system improve borrower experience?

It makes the loan journey faster and clearer. Borrowers can apply online, upload documents, track approval status, receive reminders, and manage repayments without constant follow-ups or branch visits.

6. What mistakes should lenders avoid when choosing an LMS?

Common mistakes include choosing only based on price, ignoring compliance needs, skipping API integration checks, underestimating collections workflows, and selecting software that cannot scale as loan volume grows.

7. How can a modern LMS support growth in India and the US?

A modern LMS supports growth by adapting to local payment rails, compliance rules, borrower expectations, and reporting needs. For India, that may include UPI and Account Aggregator. For the US, it may include ACH, credit bureaus, and flexible servicing workflows.