Top Loan Management Software in 2026

- Arpan Desai

- May 20

- 9 min read

Updated: May 20

Table of Content:

A loan officer in Ohio told us something recently that stuck with us. "I didn't get into lending to chase paperwork," she said. "I got into it to help people buy their first home."

Sound familiar?

The truth is, most lenders didn't sign up to wrestle with clunky systems, manual data entry, and compliance checklists that seem to grow longer every quarter. You got into this business to make an impact — for your borrowers, your team, and your community.

But here's the thing: the right loan management software gives you that time back. And in 2026, the gap between lenders who've embraced modern tools and those who haven't is wider than ever.

This guide is your shortcut to the right side of that gap.

Introduction: Why Loan Management Software Matters in 2026

Picture this: A borrower applies for a loan at 11 PM on a Sunday. They want an answer fast. Your team is asleep. Your competitors? Their loan management software is already analyzing the application, running credit checks, and sending an automated approval — all before your Monday morning coffee.

That's the world we live in now.

The lending landscape in 2026 has shifted dramatically. Borrowers expect speed, transparency, and digital-first experiences. Lenders who still rely on manual processes aren't just slow — they're invisible. According to industry reports, over 73% of borrowers will abandon a loan application if the process feels outdated or takes too long.

A modern loan management solution isn't a luxury anymore. It's the backbone of every competitive lending operation, from mortgage companies to payday lenders to enterprise banks.

Key Challenges in Loan Processing Today

Before we celebrate the solutions, let's acknowledge the mess. Loan processing in 2026 still comes with real headaches:

Manual Data Entry Errors — Human error in loan documentation can cost lenders thousands in compliance penalties. One wrong digit, one missed field, and suddenly you're explaining yourself to regulators.

Slow Approval Cycles — Traditional loan processing can take days or even weeks. Borrowers won't wait. They'll just walk across the street (digitally speaking) to your competitor.

Compliance & Regulatory Pressure — U.S. lending regulations continue to evolve. Keeping up with TILA, RESPA, ECOA, and state-specific rules without a dedicated loan management system is like trying to juggle chainsaws. Possible? Maybe. Advisable? Absolutely not.

Fragmented Systems — Many lenders still use a patchwork of tools — one for origination, another for servicing, a third for reporting. These systems don't talk to each other. Data gets lost. Teams get frustrated.

Fraud Detection Gaps — Without real-time monitoring and AI-powered alerts, catching fraudulent applications before funding is nearly impossible at scale.

A centralized lending management system solves most of these problems in one shot. But not all platforms are created equal — and that's exactly what the next section digs into.

Essential Features of Modern Loan Management Software

When evaluating any online loan management system, don't get distracted by flashy UI demos. Focus on what actually moves the needle:

Automated Loan Origination — From application intake to document collection to credit decisioning, automation should handle the repetitive work. Your team should focus on relationships, not data entry.

Real-Time Loan Monitoring — A solid loan monitoring system gives you live visibility into every loan in your portfolio — delinquencies, payment statuses, upcoming maturities. No more guessing games.

Configurable Workflows — Every lender operates differently. Your software should adapt to your process, not the other way around. Look for drag-and-drop workflow builders and rule-based automation.

Compliance Management — Built-in regulatory checks, audit trails, and auto-generated disclosures are non-negotiable for any U.S.-based lender.

Integrated Reporting & Analytics — Good data is only useful if you can understand it. Your loans management system should deliver dashboards that actually make sense — not just pretty charts that say nothing useful.

Borrower Self-Service Portal — Borrowers want to check balances, make payments, and upload documents without calling your office. A web-based portal isn't optional in 2026.

Third-Party Integrations — Credit bureaus, payment processors, core banking systems, CRMs — your web based loan management system should connect seamlessly with your existing tech stack.

Benefits of Using Loan Management Software for Lenders

Still need convincing? Here's what lenders actually experience after implementing a modern loan management system:

Faster Processing Times — Automated underwriting and document verification can cut loan approval times from days to hours. Some lenders report a 60–70% reduction in processing time.

Reduced Operational Costs — Less manual work means fewer operational bottlenecks and lower staffing costs for routine tasks. That's money that goes straight back to your bottom line.

Better Borrower Experience — Faster approvals, transparent communication, and digital-first interactions lead to higher borrower satisfaction and stronger referral rates.

Improved Portfolio Quality — With real-time risk scoring and loan monitoring system capabilities, lenders can catch early warning signs before a loan goes bad.

Scalability — Whether you're processing 50 loans a month or 5,000, the right loan management systems scale with your volume without breaking a sweat.

Regulatory Confidence — Built-in compliance tools mean fewer audit surprises and greater confidence during examinations.

The ROI on quality lending software isn't theoretical — it shows up in your quarterly numbers.

How AI and Automation Are Shaping Loan Management

If 2024 was the year everyone talked about AI, 2026 is the year lenders are actually using it — profitably.

Here's what artificial intelligence is doing inside modern loan management software right now:

Predictive Credit Scoring — AI models analyze thousands of data points beyond the traditional FICO score — payment behavior patterns, cash flow data, even social and business signals — to produce more accurate risk assessments.

Automated Document Processing — OCR and machine learning can now extract, verify, and classify loan documents in seconds. Tax returns, bank statements, pay stubs — processed automatically with minimal human touchpoints.

Fraud Detection — AI-powered anomaly detection flags suspicious application patterns in real time, protecting lenders before funding occurs.

Chatbots & Virtual Assistants — Borrowers can get instant answers to their loan status questions 24/7 without tying up your team. Everybody wins.

Dynamic Pricing Models — AI helps lenders adjust interest rates based on real-time risk data, market conditions, and borrower profiles — maximizing yield while staying competitive.

Lenders who embrace these capabilities aren't just more efficient. They're fundamentally more intelligent businesses. And for specialized segments like short-term lending, payday loan management systems with embedded AI are transforming how those portfolios are underwritten and monitored.

Top Loan Management Software Solutions in 2026

Now, the part you've been scrolling for. Here are some of the most talked-about platforms in the U.S. lending market right now:

Fintegration Loan Management System — A powerful, flexible loan management solution built for lenders who need customization without compromising on compliance. Fintegration's platform supports everything from origination to servicing, with robust reporting, borrower portals, and seamless integrations. Their custom lending software solutions are particularly well-suited for lenders who've outgrown off-the-shelf tools and need something built around their specific workflows.

Encompass by ICE Mortgage Technology — A longtime favorite in the mortgage space, Encompass offers deep compliance features and broad integrations, though its learning curve can be steep for smaller teams.

TurnKey Lender — Popular among mid-sized lenders and credit unions, TurnKey Lender offers a cloud-based lending management system with AI-driven underwriting and solid borrower-facing features.

LoanPro — A highly configurable cloud platform known for its developer-friendly API and strong loan servicing capabilities. Particularly popular with fintech lenders building proprietary products on top of a solid infrastructure.

Nucleus Software — Strong in the commercial and corporate lending segments, Nucleus brings enterprise-grade capabilities with deep analytics and multi-currency support — useful for U.S. lenders with international exposure.

LOAN IQ by Finastra — Built for syndicated and complex commercial loans, LOAN IQ is the go-to for large financial institutions managing intricate loan portfolios.

Each platform has its strengths, and the right choice depends entirely on your loan type, volume, team size, and growth plans.

Choosing the Right Software for Your Business Needs

Here's where most buying decisions go wrong: lenders get dazzled by demos and forget to ask the questions that actually matter.

Before you sign anything, run through this checklist:

What loan types do you handle? — Consumer, mortgage, commercial, SBA, auto, payday? Not every platform handles every product equally well. Confirm your specific loan types are fully supported.

What's your monthly volume? — A boutique lender doing 30 loans a month has very different needs than a regional bank doing 3,000. Match the platform's architecture to your scale.

How much customization do you need? — Some businesses need a plug-and-play solution. Others need a lending management system that bends to their process. Know which camp you're in before evaluating.

What does your current tech stack look like? — Integration capabilities matter enormously. Make sure your prospective platform connects cleanly with your core banking system, CRM, and payment rails.

What does implementation look like? — Ask vendors for realistic timelines and get references from clients of similar size and complexity. Vendors who can't provide references are a yellow flag.

What's the total cost of ownership? — Look beyond licensing fees. Factor in implementation, training, ongoing support, and customization costs.

The best loan management systems don't just check feature boxes — they become a genuine operational advantage.

Case Studies: Success Stories from Leading Lenders

Community Credit Union — Midwest, USA A 12-branch credit union was managing their loan portfolio through a combination of spreadsheets and a legacy system that hadn't been updated since 2015. After implementing a modern online loan management system, they reduced loan processing time by 58%, cut operational costs by 31%, and saw borrower satisfaction scores jump by 22 points within the first year.

Regional Commercial Bank — Southeast, USA A regional bank specializing in small business loans was struggling with compliance documentation. Every audit was a scramble. After deploying a compliant loan management system with automated audit trails and regulatory reporting, their last two examinations were described by examiners as "remarkably clean." That's not a phrase banks hear often — and they loved it.

Fintech Startup — California A consumer lending startup needed a scalable infrastructure to support rapid growth. Rather than building from scratch, they partnered with a provider offering custom lending software solutions that integrated with their mobile app. Within 18 months, they scaled from 200 to 4,000 monthly applications without adding proportional headcount.

These aren't outliers. They're what happens when the right technology meets a team ready to use it.

Future Trends: What's Next in Loan Management Software

The pace of change in lending technology isn't slowing down. Here's what smart lenders are watching for the next two to three years:

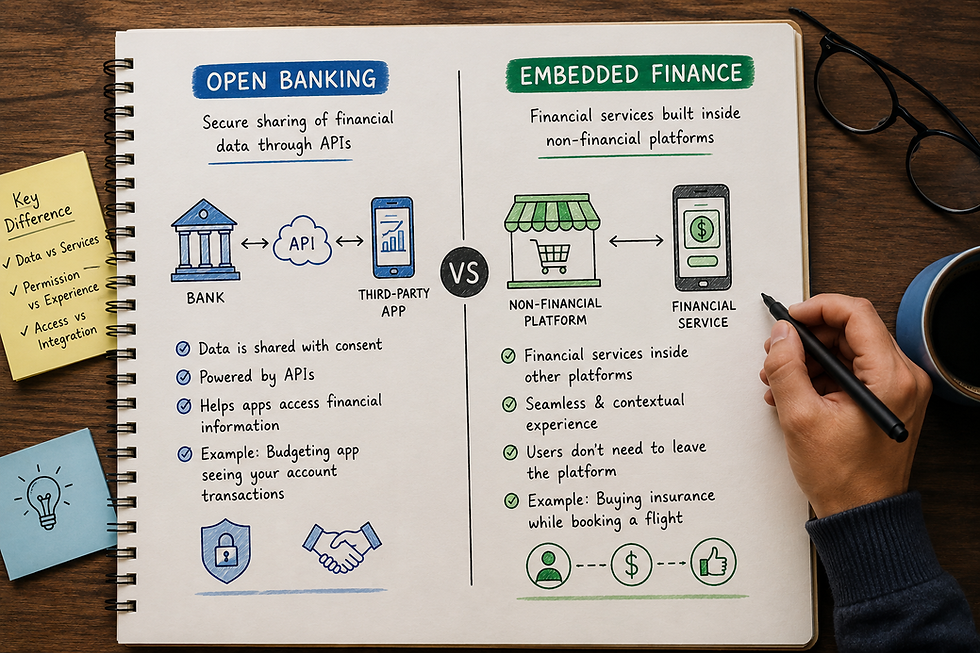

Embedded Lending — Loans are increasingly being offered at the point of need — inside e-commerce platforms, accounting software, and business tools. The underlying engine is always a modern loans management system operating invisibly in the background.

Open Banking Integration — Real-time access to borrower financial data (with consent) is transforming underwriting accuracy and speed. Expect this to become standard in U.S. lending workflows.

Blockchain for Loan Documentation — Immutable, verifiable loan records on distributed ledgers are moving from concept to pilot across several major institutions. It's not mainstream yet — but it's coming.

Hyper-Personalized Loan Products — AI will enable lenders to craft loan terms dynamically — rates, repayment schedules, and structures tailored to individual borrower profiles in real time.

ESG Lending Metrics — Environmental and social governance factors are increasingly influencing commercial lending decisions. Software platforms will need to track and report these metrics as regulatory pressure grows.

Lenders who invest in adaptable, API-first platforms today are positioning themselves to absorb these changes without needing a full system overhaul every few years.

Conclusion

Here's the bottom line: the lending market in 2026 rewards speed, intelligence, and borrower experience. Manual processes and fragmented systems are no longer just inefficient — they're actively costing you business.

The right loan management software doesn't just automate tasks. It transforms how your team operates, how your borrowers experience your brand, and ultimately, how your portfolio performs.

Whether you're exploring a full platform replacement or looking to modernize specific parts of your lending workflow, the key is to start with clarity — know your loan types, your volume, your compliance obligations, and your growth ambitions. Then find a platform that genuinely fits.

If you're looking for a flexible, scalable, and deeply customizable solution, Fintegration's loan management system and their custom lending software solutions are worth a serious look — especially if your needs go beyond what off-the-shelf software can handle.

The lenders winning in 2026 aren't the biggest ones. They're the smartest ones. And now you know exactly what smart looks like.

FAQ

1. What is loan management software and why do I need it in 2026?

Loan management software is a digital tool that helps lenders track, process, and manage loans efficiently. In 2026, it’s essential because it reduces manual work, minimizes errors, and speeds up approvals while improving customer experience.

2. How does loan management software simplify loan processing?

It centralizes borrower information, automates calculations, schedules repayments, and tracks loan performance. This means less paperwork, fewer mistakes, and more time for lenders to focus on strategic decisions.

3. What are the must-have features in top loan management software?

Look for automated workflows, AI-powered risk assessment, real-time reporting, compliance tracking, secure document storage, and seamless integration with banking and payment systems.

4. Can small lenders benefit from loan management software too?

Absolutely! Even small lending businesses can save time and reduce errors with automation. Modern cloud-based solutions are scalable and cost-effective, making them accessible for any size lender.

5. How does AI improve loan management in 2026?

AI can analyze borrower data for creditworthiness, detect fraud patterns, predict repayment risks, and optimize workflows. This ensures smarter decisions and faster approvals without sacrificing accuracy.

6. How do I choose the right loan management software for my business?

Consider your loan types, regulatory requirements, team size, integration needs, and budget. Demo multiple solutions to see which one fits your workflow, provides strong support, and is easy to use.

7. Will loan management software help improve customer satisfaction?

Yes. By streamlining processes, providing transparent updates, and reducing delays, borrowers experience faster approvals and smoother interactions, building trust and long-term loyalty.