How to Create a Secure and Efficient Payment Gateway?

- Nishant Shah

- Jan 24, 2024

- 7 min read

A secure and efficient payment gateway is built by combining encrypted payment processing, tokenization, PCI DSS-aligned security controls, fraud detection, reliable processor integrations, and a fast checkout experience. It should also support idempotency, transaction monitoring, refunds, dispute handling, reporting, and fallback mechanisms to prevent duplicate charges and reduce payment failures. |

Creating a payment gateway that is both secure and efficient is essential for any financial institution or fintech startup operating in the USA. A payment gateway acts as the bridge between customers, merchants, and banks, enabling smooth and safe transactions. In this post, we will explore the key steps and best practices to build a payment gateway that meets the highest standards of security and performance.

Understanding the Role of a Payment Gateway

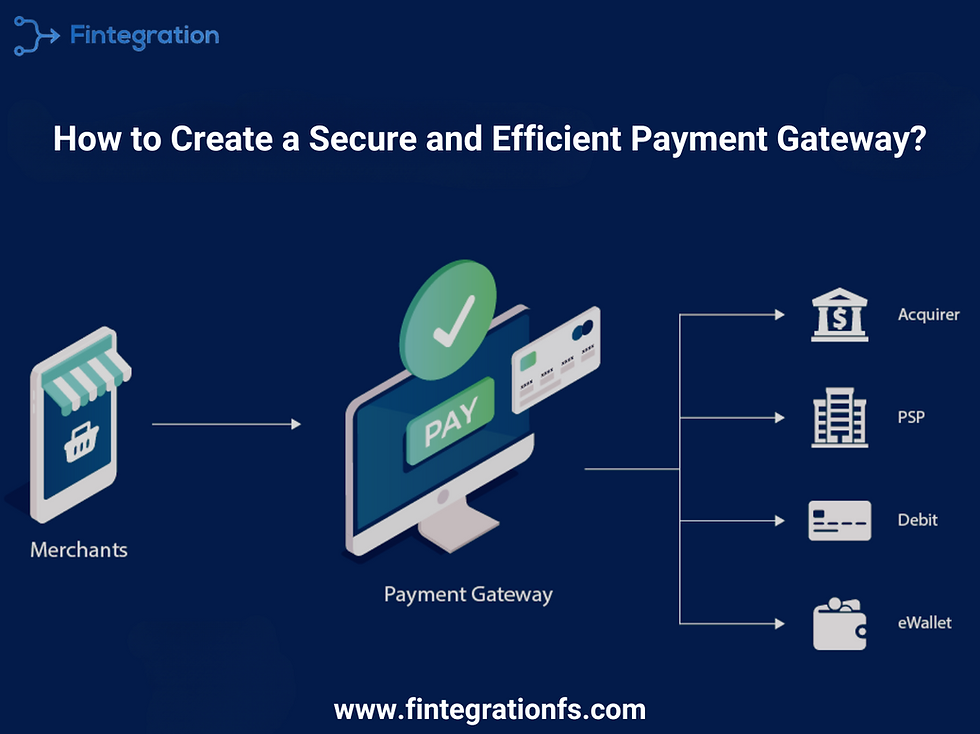

A payment gateway processes payment information from customers and communicates with banks or payment processors to authorize and complete transactions. It handles sensitive data such as credit card numbers, bank account details, and personal information. Because of this, security is a top priority.

Efficiency is equally important. Customers expect fast, seamless payment experiences without delays or errors. A slow or unreliable payment gateway can lead to lost sales and damage to reputation.

Key Components of a Secure Payment Gateway

To build a secure payment gateway, focus on these core components:

Data Encryption: Use strong encryption protocols like TLS (Transport Layer Security) to protect data during transmission. This prevents interception by unauthorized parties.

Tokenization: Replace sensitive payment data with tokens that have no exploitable value. This reduces the risk of data breaches.

PCI DSS Compliance: Follow the Payment Card Industry Data Security Standard to ensure your system meets industry security requirements.

Fraud Detection: Implement real-time fraud monitoring tools to identify suspicious transactions and prevent chargebacks.

Secure Authentication: Use multi-factor authentication (MFA) for users accessing the payment gateway backend.

Regular Security Audits: Conduct frequent vulnerability assessments and penetration testing to identify and fix security gaps.

Building an Efficient Payment Gateway

Efficiency depends on several factors:

Optimized Transaction Flow: Minimize the number of steps a customer must take to complete a payment.

High Availability: Design the system to handle high volumes of transactions without downtime.

Fast Processing: Use scalable infrastructure and optimized code to reduce transaction latency.

Multiple Payment Methods: Support credit cards, debit cards, digital wallets, and ACH payments to cater to diverse customer preferences.

Clear Error Handling: Provide informative error messages and retry options to avoid transaction failures.

Choosing the Right Technology and Partners

Selecting the right technology stack and partners can make or break your payment gateway project. For example, FintegrationFS offers a comprehensive platform that supports secure, compliant, and scalable fintech products. Their expertise in AI-native engineering helps build payment gateways that meet regulatory requirements and deliver excellent user experiences.

Another example is Stripe, a popular payment gateway provider known for its developer-friendly APIs and strong security features. Stripe supports multiple payment methods and offers built-in fraud detection tools.

PayPal is also a widely used payment gateway with a strong reputation for security and ease of integration. It supports a broad range of payment options and provides buyer and seller protection.

Comparing these options can help you decide whether to build your own gateway or integrate an existing solution. For fintech startups and financial institutions aiming to innovate quickly, partnering with a provider like FintegrationFS can accelerate development while ensuring compliance and security.

Steps to Create Your Payment Gateway

Here is a step-by-step approach to building a secure and efficient payment gateway:

Define Requirements

Identify the payment methods, currencies, and countries you will support. Understand your target users and transaction volumes.

Design System Architecture

Plan a modular architecture that separates payment processing, fraud detection, user management, and reporting.

Implement Security Measures

Integrate encryption, tokenization, and authentication from the start. Ensure PCI DSS compliance.

Develop Core Features

Build APIs for payment authorization, capture, refunds, and cancellations. Include support for multiple payment methods.

Integrate Fraud Detection

Use machine learning models or third-party services to monitor transactions in real time.

Test Thoroughly

Perform functional, security, and load testing to ensure reliability and safety.

Deploy and Monitor

Launch your gateway with monitoring tools to track performance and security incidents.

Best Practices for Payment Gateway Security

Security is an ongoing effort. Follow these best practices:

Keep Software Updated

Regularly patch your systems and libraries to fix vulnerabilities.

Limit Data Access

Use role-based access control to restrict who can view or modify sensitive data.

Encrypt Data at Rest and in Transit

Protect data stored in databases and during communication.

Use Strong Password Policies

Enforce complex passwords and MFA for all users.

Monitor Logs

Analyze logs for unusual activity and respond quickly to incidents.

Educate Your Team

Train developers and staff on security best practices and compliance requirements.

Enhancing User Experience in Payment Gateways

A secure gateway must also be user-friendly. Consider these tips:

Simplify Checkout

Reduce the number of fields and steps required to complete payment.

Mobile Optimization

Ensure the gateway works smoothly on smartphones and tablets.

Provide Multiple Payment Options

Let customers choose their preferred payment method.

Offer Clear Feedback

Show progress indicators and confirmation messages.

Support Multiple Languages and Currencies

Cater to diverse users, especially if you plan to expand beyond the USA.

Leveraging AI and Automation

AI can improve both security and efficiency. For example, FintegrationFS uses AI-native engineering to build fintech products that adapt to changing threats and optimize transaction flows. AI-powered fraud detection can spot patterns humans might miss. Automation can speed up compliance checks and reporting.

Final Thoughts on Building a Payment Gateway

Building a secure and efficient payment gateway requires careful planning, strong security measures, and a focus on user experience. Whether you choose to develop your own system or partner with providers like FintegrationFS, Stripe, or PayPal, the goal is to create a reliable platform that customers trust and enjoy using.

By following the steps and best practices outlined here, you can build a payment gateway that supports your business goals and meets the high standards expected in the US financial market.

Secure payment processing is the backbone of modern fintech. Let’s build gateways that protect data, speed transactions, and open new opportunities for financial innovation.

FAQ

1. What is a payment gateway, and how does it work?

A payment gateway is the technology that securely transfers payment information between the customer, merchant, payment processor, card network, and issuing bank.

When a customer enters card or bank details, the payment gateway encrypts the information, sends it for authorization, and returns an approved or declined response. This usually happens within a few seconds, making the checkout experience feel simple even though several systems are communicating behind the scenes.

2. What are the main steps for creating a payment gateway?

Creating a payment gateway usually involves defining the business model, selecting supported payment methods, designing the system architecture, integrating processors or banking partners, implementing security controls, building merchant and admin dashboards, and testing the full transaction flow.

The project should also cover compliance, fraud prevention, refunds, disputes, reconciliation, reporting, and failed-payment handling. A successful payment gateway is not only able to process payments. It must also manage everything that can happen before and after a transaction.

3. What security features should a payment gateway include?

A secure payment gateway should include encryption, tokenization, strong access controls, multi-factor authentication, secure API authentication, transaction monitoring, audit logs, and fraud-detection rules.

Sensitive payment details should never be stored unnecessarily. The payment gateway should also protect against common threats such as account takeover, card testing, replay attacks, API abuse, and unauthorized administrative access.

4. Does a payment gateway need to comply with PCI DSS?

A payment gateway that stores, processes, or transmits cardholder data may need to meet applicable PCI DSS requirements.

The exact compliance scope depends on how the payment gateway is designed and which third-party providers are involved. Using tokenization, hosted payment fields, or an external processor can reduce the amount of sensitive data handled directly by the platform, but it does not remove every security and compliance responsibility.

A qualified compliance professional should review the final architecture and data flow.

5. How can tokenization improve payment gateway security?

Tokenization replaces sensitive payment information with a non-sensitive token. The payment gateway can use that token for future transactions without repeatedly storing or exposing the customer’s original card details.

This reduces the impact of a potential data breach and can simplify recurring payments, saved cards, subscriptions, and one-click checkout experiences. The token should still be protected because it may be valuable within the payment ecosystem.

6. How do you make a payment gateway fast and efficient?

A payment gateway can be made more efficient through optimized APIs, reliable processor connections, intelligent routing, asynchronous processing, caching where appropriate, and well-designed database operations.

The platform should also use timeouts, retries, idempotency controls, and fallback routes carefully. These features help prevent duplicate charges and reduce failed transactions when a bank, processor, or external service is temporarily unavailable.

Efficiency should never come at the expense of payment security or accurate transaction records.

7. How can a payment gateway prevent fraud?

A payment gateway can reduce fraud by combining transaction rules, device signals, velocity checks, location analysis, identity verification, behavioral patterns, and machine-learning risk scoring.

For example, the system may flag repeated payment attempts, unusual transaction amounts, mismatched billing information, or sudden activity from a new device.

Fraud controls should be adjustable because overly strict rules may block legitimate customers. The goal is to reduce risk without creating unnecessary friction at checkout.

8. What payment methods can be supported by a payment gateway?

A payment gateway may support credit cards, debit cards, ACH payments, digital wallets, bank transfers, real-time payment methods, buy-now-pay-later services, and local payment options.

The right payment methods depend on the target market, customer preferences, average transaction value, and business model. Supporting every payment method from day one is not always necessary. Many businesses begin with the most important options and expand based on customer demand.

9. How long does it take to build a payment gateway?

The timeline for building a payment gateway depends on the required features, supported markets, compliance scope, payment methods, processor integrations, and level of customization.

A focused payment solution using established providers may take a few months. A more advanced payment gateway with multi-currency support, smart routing, merchant onboarding, settlement management, fraud systems, and custom reporting can take considerably longer.

Security reviews, banking approvals, certification, and real-world testing often influence the launch timeline.

10. Should a business build a custom payment gateway or use an existing provider?

Using an existing provider is often the faster option for businesses that need standard payment processing and want to reduce infrastructure and compliance work.

A custom payment gateway may make sense when the business needs specialized transaction flows, multi-processor routing, unique pricing rules, deeper platform control, or payment functionality that existing providers cannot support effectively.

Before building, compare development cost, maintenance, compliance responsibilities, scalability, vendor dependence, and long-term transaction economics. In many cases, a hybrid approach offers the best balance between speed and control.